Categories

Indians are obsessed with owning gold and houses. And it’s not just a recent or Indian phenomenon. Hear it from one of the richest persons ever lived.

“Ninety percent of all millionaires become so through owning real estate.” – Andrew Carnegie

Even though the quote is dated, and we certainly won’t comment on the accuracy of the 90%, these words surely do tell the importance of real estate as an investment. In economic theory, the land is one of the three means of production, the other two are capital and labour.

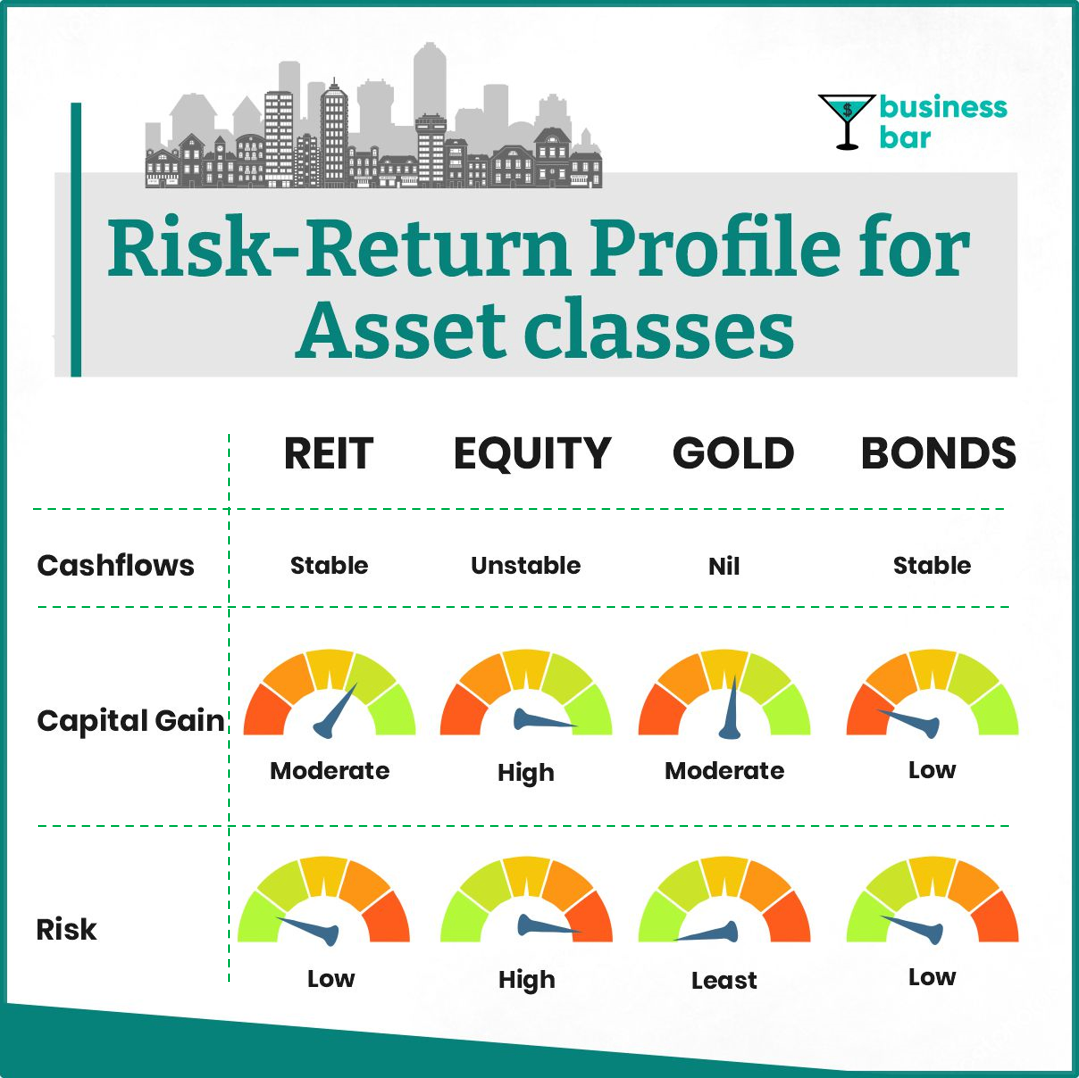

What is the reason that investors till date invest in real estate? The answer is a long list: Regular and stable rental income, capital appreciation, tax deductions, hedge against inflation and portfolio diversification. In a downturn, when the stock market has low or negative returns, Real Estate investments can give stable returns.

Categories of real estate:

But owning real estate can be expensive and maintenance-intensive, especially in the case of commercial buildings. To solve this, in the 1960s, the US established REITs with the objective of providing a channel to small retail investors where they can invest in income-producing real estate. REIT allows retail investors like you and us to have exposure to this asset class without the hassle of maintaining the property and shedding lacs (or crores) of rupees on the down payment.

For the uninitiated, REIT (Real Estate Investment Trust) is a company that owns, operates or finances income-producing real estate. REIT owns a pool of properties. Think of the REIT as a Mutual Fund and the pool of properties as a portfolio of stocks. A unit of Mutual Funds gives you a claim to the net assets of the fund, similarly, a share of REIT gives you a claim on the pool of properties, the rental income, and the long term capital appreciation.

REITs have characteristics of both the equity market as well as fixed-income investments. The fixed-income investment gives stable interest income and reduced downside risk. Equity investments give upside potential, dividends, and liquidity for retail investors. REITs are mandated to distribute 90% of income to shareholders thus giving stable income like fixed income. They also have growth opportunities driven by rental income revision and asset appreciation like equity markets.

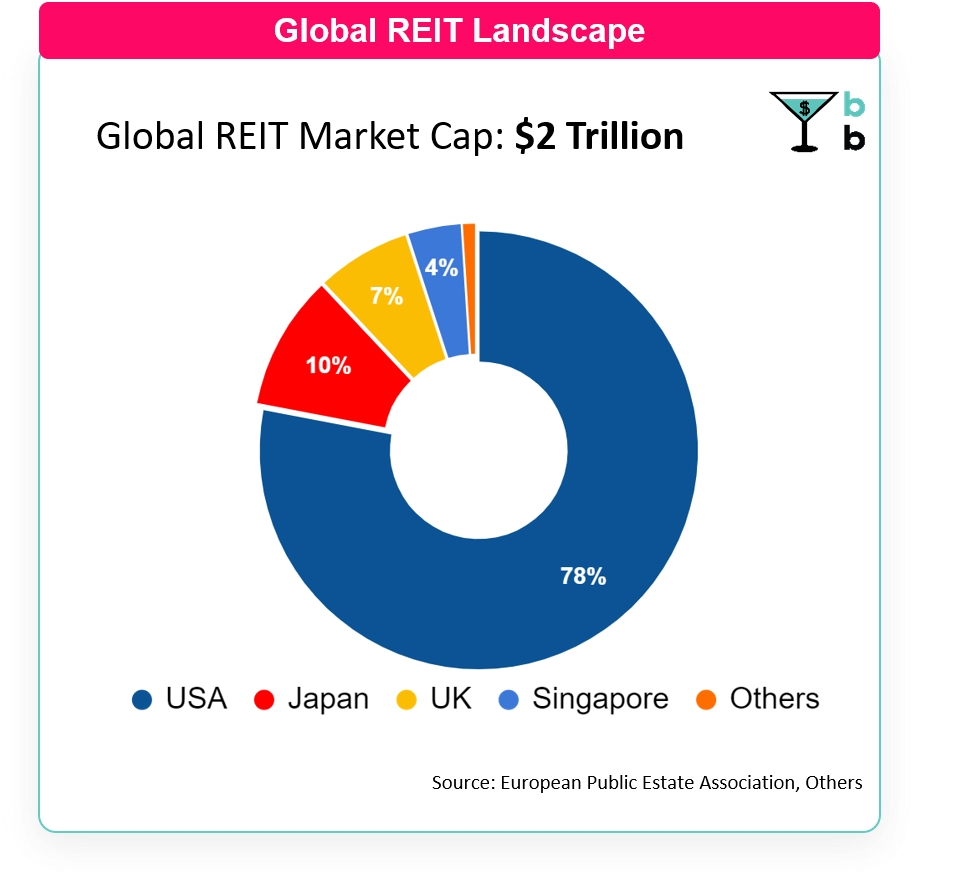

So, a publicly listed REIT allows all types of investors to invest in income-producing real estate properties like offices, hotels, and apartments. Today, there are around 500 REITs globally. According to estimates of the European Public Estate Association, the total value of listed real estate globally is around $3.8 trillion. Property under REITs forms nearly 53%, around $2 trillion. However, this is largely concentrated in developed markets.

The USA was the first mover into the REITs, and it’s a no-brainer that the real estate market of the United States is most mature. Remember the 2008 financial crisis. The US housing market was on steroids and hundreds of billions of dollars went into all kinds of exotic financial instruments betting on the US housing market.

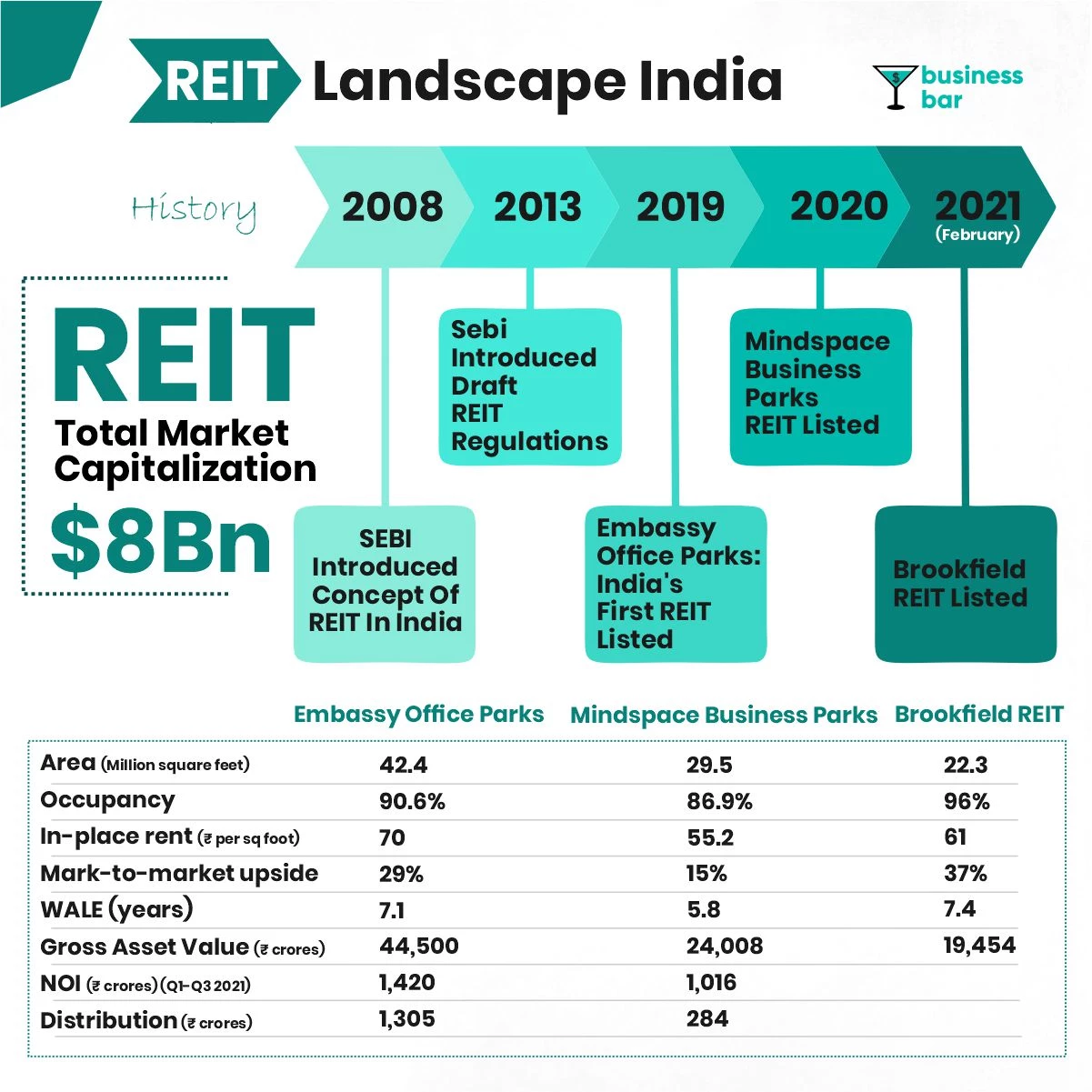

However, it took almost 50 years for SEBI to finally introduce REIT in India and the first REIT offering was launched in 2019.

SEBI introduced the concept of REITs as a new investment vehicle for the first time in February 2008. Five years later SEBI issued draft regulations for REITs in 2013 and later amended and finalised in 2017.

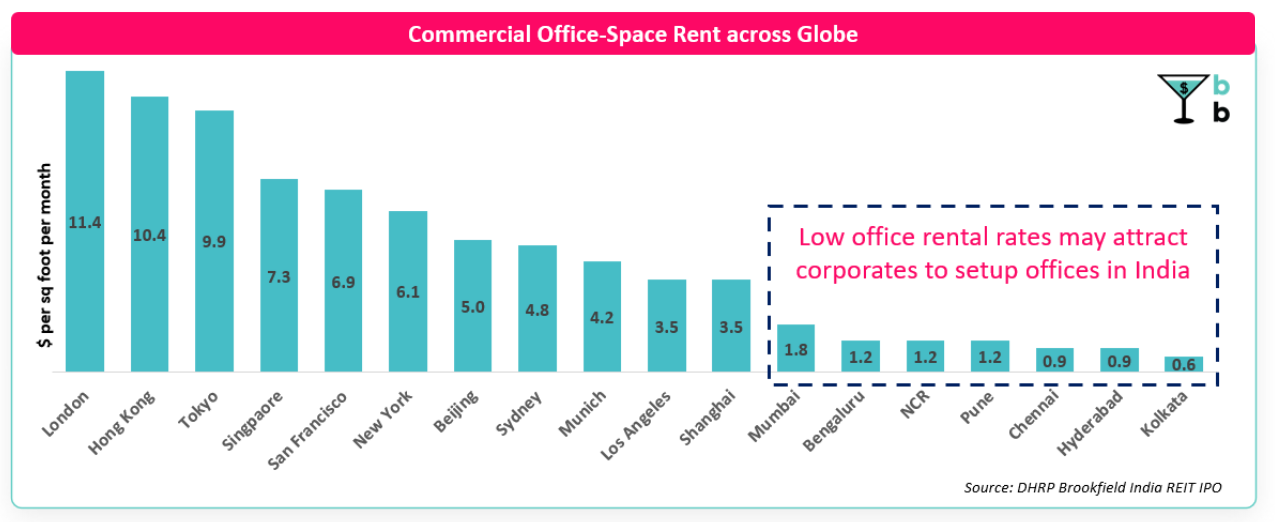

Currently, India’s real estate sector is the second-largest employer in the country after agriculture. The Indian real estate sector attracted USD 43.5 Bn of institutional investments during 2016-20, nearly 5 times the investment of USD 9.4 Bn made in the previous five years. Out of the total USD 43.5 Bn received, around $14 Bn came from foreign PE investors. The office leasing space in India is 60.6 million square foot across 8 major cities and demonstrated a growth of 27% in 2019.

On 1st April 2019, India’s first REIT – Embassy Office Parks – was listed. This was a big step for the Indian real estate landscape. This introduced the investors at home and abroad to a new investment opportunity in India. The offering opened at Rs 300 per share and was oversubscribed 2.5 times.

With this, the gates were opened. Even in the post-pandemic era, the investing trend continued. In August 2020, Mindspace Business Parks was listed on stock exchanges. The issue was oversubscribed 13x. The industry witnessed a $2Bn deal of Brookfield Asset Management buying 12.5 million square feet of commercial real estate from RMZ corp. This was followed by the third REIT issue: Brookfield REIT in Feb 2021.

One of the biggest factors that have worked in the case of all the three listed REITs is the backing of global PE firms. Embassy Office Parks and Mindspace Business Parks are led by Blackstone Group, whereas the latest issue of Brookfield Real Estate Investment Trust is led by Brookfield Asset Management. It doesn’t get better than this. Now, if you are wondering how the three REITs fare against one other, no worries, we have got you covered.

If you are unfamiliar with any of the terms, here is a quick glossary:

In India, for a company to be qualified as REIT, they need to meet the following criteria set up by regulators:

So, you can see it’s not that easy to set up a REIT. Well, all of this is not hunky-dory. And as you would have guessed, the pandemic impacted the REIT industry as well.

Real Estate derives its value on the basis of cash flow (rental income) it can generate. And as the pandemic hit, everything shifted on a work from home model. Offices became empty. The big business parks became deserted.

“The fallout from Covid has caused rents, occupancies, and prices to take a tumble,” – Green State (Research firm specializing in Real Estate)

Short term effects on REITs were seen with Indian REITs as well. The Embassy Office Parks is currently trading close to the issue price of Rs 300 per share compared with a pre-covid all-time high of Rs. 470. Brookfield REIT is also trading at a discount as of February end 2021.

Luckily, for India, all the three listed REITs own Grade A property assets. They had excellent rent collection during the lockdown as well. Two of these three REITs were listed post-Covid outbreak.

Though safer than the stock market, REITs do come with certain risks. Especially during a downturn, the risk of vacancy increases. On part of an investor, risk is also associated with choosing REIT. If a REIT has properties where there is low demand (think abandoned malls), it means diminished or even negative returns.

The debut of REIT in the Indian market has brought much-needed liquidity into the real estate sector. The real estate sector has been facing a deep liquidity crunch for some years now. REIT also allows an additional lifeline for the inflow of capital from foreign investors as well as domestic investors.

“International pension funds, sovereign funds, education funds, ETFs are investing in REITs in India. We have certainly seen our investor base deepen over time. Even domestically, retirement funds are deploying money in REITs.” – Mike Holland, CEO of Embassy Office Parks

The Indian REIT market is pretty nascent when compared with some of the developed markets like the US, Hongkong and Singapore. REIT IPOs have traditionally accounted for 32% of the total IPO volumes in Singapore. The market cap of Singapore office Reits would be an estimated $75-80 billion, while in India it is $8bn after the 3rd listing.

The majority of Grade-A offices in India are occupied by European and American multinational companies. Due to a demand for quality office space, the rental income has grown by 5% YoY over the last 5 years. Even though the pandemic has thrown up some challenges for the real estate market, the medium and long term trend for the commercial real estate sector looks quite favourable. This is due to macroeconomic conditions, the supply of engineers, growth of the technology sector and competitive cost with quality office space. The rent collection rate for Embassy Office Parks was 95% in April 2020 indicating a positive sentiment towards this space.

The government and SEBI are also keen on expanding this sector. The trading lot size for REITs has been halved to increase retail participation. Simplifying business activities, and slashing effective tax rates for corporates from 34.5% to 25.2% would also boost the sector.

The office sector will remain integral for the next few years. But going forward, the REIT landscape will further evolve to include other types of assets and properties. The biggest potential lies in front of public sector companies though. Indian PSUs are sitting on vast assets of land and a REIT can unlock this potential by monetizing the land assets.

This article is co-written by Nevil Kathiria