Categories

The coronavirus pandemic has ravaged countries in large and small across the globe, impacting businesses across sectors. The pharmaceutical sector was no exception to this. In the pharmaceutical industry, Indian drug manufacturers faced the supply chain disruptions and issues around logistics, but as the saying goes – adversity and hard times bring out the best in us.

While the whole world is fighting a battle against the pandemic with an increased focus on people’s health, health systems around the world face intense pressure from escalating demand. To counter the spread of coronavirus, every country is now in a race to find a durable cure for COVID-19 (in the run-up to a vaccine) that would permit them to restart economic activity.

Recently, the Indian pharma sector has been in the news globally as India will play a pivotal role in developing and scaling of COVID-19 vaccines. To understand this, we have mapped the journey of the Indian pharma industry, the impact of Chinese conflict on the sector, and the road ahead.

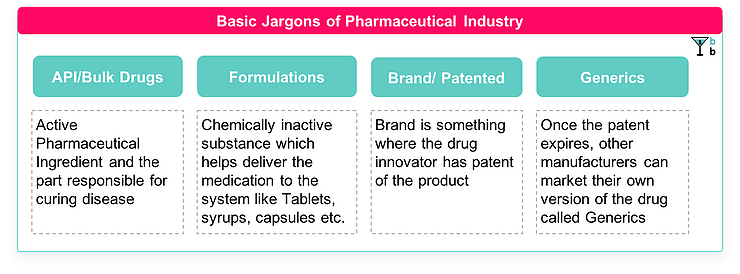

Before you begin, we recommend you familiarize yourself with these basic pharma jargons. It will come handy, especially if you don’t have a pharma background.

From Rags to Riches

The Indian pharmaceutical industry has witnessed many twirls and swirls in the last five decades. Like the other emerging economies in the 70s, India was ‘vulnerably’ dependent on the west for its pharma needs – be it formulations or APIs. From being nowhere on the global pharma map in 1970 to now playing a key role in delivering high-quality and affordable generic drugs worldwide, the Indian pharma industry has come a long way.

It began with the Indian Patents Act 1970. It is widely lauded for facilitating the growth of the Indian pharma industry. The act forms the basis of the country’s intellectual property regime as it removed product patent protection in pharmaceuticals. The domestic companies adopted the ‘reverse engineering process’ to manufacture drugs without paying any royalty to the patent holders (drug innovator). This led to a golden era for the industry.

Reverse Engineering: Reproduction of another manufacturer’s product following a detailed examination of its formula or composition

Over the years, Indian manufacturers have developed considerable expertise in reverse engineering of drugs. The Indian companies just copied the drug formula, saved big bucks on royalty and R&D (millions of dollars and years of research). As a result, Indian manufacturers kept drug prices economical. The domestic companies could sell drugs at as little as one-tenth of the original prices! Indian manufacturers were particularly well placed to export these generic medicines to the rest of the world.

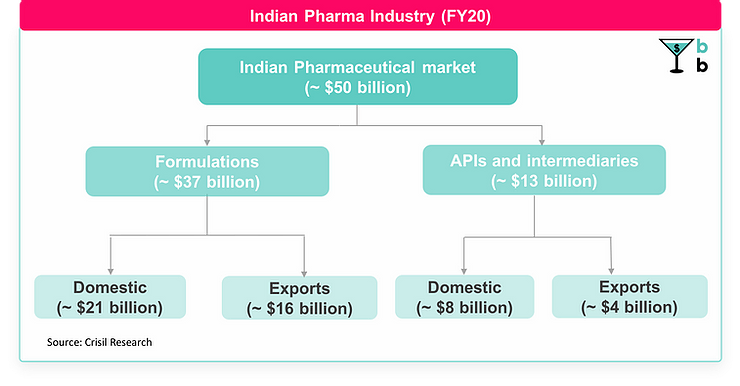

This was a paradigm shift for the pharma industry. Five decades ago, India was an importer of everything and anything, when it came to our pharmaceutical needs. India has managed to reverse this equation. Today, India’s pharma sector is robust and thriving. As of 2020, it is estimated to be more than a $50 Bn industry – vertically divided into domestic and exports. India is the biggest supplier of generics globally. And India has rightfully earned the epithet ‘Pharmacy to the World.’

“India is capable of producing Covid-19 vaccine for the entire world”

– Bill Gates

The Indian pharmaceutical industry is the world’s third-largest in terms of volume and thirteen largest in terms of value. More vaccines are made in India than anywhere. India fulfills 20 percent of global demand for generic medicines in terms of volume.

Well, all this sounds like a fairy tale, but there is a flip side. This success has come at a cost that hinders the prospects of the Indian pharma sector and thus India as a whole.

Paradox of the Indian Pharma Industry

Although India is one of the top formulation drug exporters in the world, its pharmaceutical industry relies heavily on the import of bulk drugs (APIs). Over the past two decades, India’s reliance on imports for intermediates and APIs has increased substantially. It can be largely attributed to the lack of cost-effective options in domestic API manufacturing when compared to imports.

As the industry matured and grew, Indian players gravitated towards the highly lucrative ‘formulation’ part of the value chain rather than API manufacturing. Though the manufacturing capacity for many imported APIs exists in India, manufacturers are reluctant to use their idle capacity or restart closed plants due to competitive pricing strategies.

Cheaper imports lead to a reduction in employment opportunities and tax revenue loss to the government. We’ll see how this dependence and potential supply shortage of essential drugs due to the market dynamics pose a threat to India’s drug security.

Reliance on Chinese imports hits home

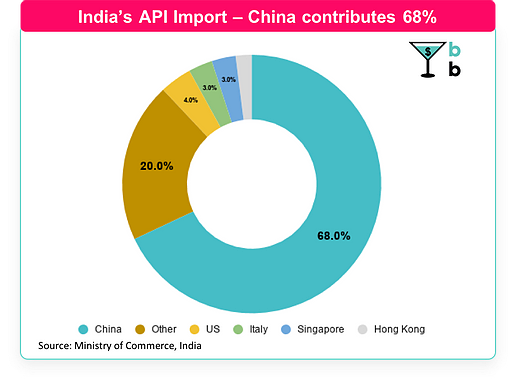

Currently, India imports nearly 68 percent of API, by value, from China. China is also the single supplier for many critical intermediaries and APIs including high-burden diseases like diabetes, cardiovascular diseases, and tuberculosis. These are also listed in the National List of Essential Medicines (NLEM). We are also dependent on China for antibiotic APIs like Penicillin.

Imports from China have been on a steady rise over the years – from 62 percent in FY12 to 68 percent in FY19. The primary reason behind the trend is the low-cost advantage enjoyed by Chinese manufacturers. With high import dependency on a single nation, we are again ‘vulnerably’ dependent. This alarms the need of India to be self-sufficient (Atma Nirbharta), especially amidst the recent conflict with the Dragon.

Are we heading towards Atmanirbhar Bharat?

Well, it has been a decade since we are aware of our stark dependence on China, but it took a global pandemic for us to realize the implications. The current outbreak of Coronavirus disrupted the supply of intermediates and APIs from China, which has resulted in supply shortages and higher cost of imports in India.

Many domestic pharmaceutical companies (Dr. Reddy’s, Torrent Pharma) have now started backward integrating into the manufacturing of APIs. However, reducing dependence on China will not be easy to achieve. Any decoupling from China must be strategic. It requires significant policy support, and it will take time for a paced indigenization. A reactive decoupling could disrupt the production of a wide range of medicines that currently require ingredients from China.

Having said that, India has a stronger starting point than most other countries given the presence of some API production capabilities at home. Recently, the government has also taken swift action to support the manufacturing of bulk drugs in India. The government has approved a package of INR 9,940 crore to boost domestic production as well as exports. It includes the establishment of bulk drug parks with common infrastructure facilities and a Production Linked Incentive (PLI) scheme. This will promote the domestic production of 53 critical ‘key starting materials’ (KSM), drug Intermediates, and APIs.

These schemes will provide the much-needed impetus to the bulk drug industry and is a step in the right direction. We are at a critical juncture now and it will be interesting to see if Indian pharmaceutical companies can ‘boycott’ and reduce dependence on Chinese raw material.

Our parting thought to you is, can India emerge as a self-reliant API manufacturing nation in times to come?

This piece is co-written by CA Sarvagya Garg