Categories

Curefit – an all-in-one fitness and health app – revolutionized the fitness industry with its unique approach. The company led by Myntra founder and ex-Flipkart executive is now eyeing to conquer the digital health space.

Led by Singapore’s Temasek, a number of investment firms committed $110 Mn in March valuing Curefit at $575 Mn and that’s more than 15x of its FY19 revenues! It was a few steps away from becoming a unicorn, but the whole picture changed after the pandemic. Will it still achieve what it aspired for or will the bubble just burst? First, we need to understand what Curefit actually is and what it has been up to.

Let us take you on time travel.

2016: Curefit Begins

Mukesh Bansal started his journey in Silicon Valley during the dotcom boom. He worked there for 8 years and returned to India to found Myntra in 2006, India’s largest fashion e-commerce site. After selling Myntra to Flipkart for $375M, Bansal and former Flipkart executive Ankit Nagori established CureFit, a health and wellness start-up with the vision to become a ‘super-app’ centered around better health. And all hail the Flipkart mafia – Kalaari Capital invested millions of dollars in not a product but in a decade long ongoing relationship.

Since its inception in 2016, Curefit has introduced multiple services to build an ecosystem of fitness, healthy food and healthcare. Starting with gyms to disrupt the conventional fitness industry, it swiftly entered into healthy food, yoga, mental wellness and primary healthcare. Recently they have also added categories like fitness wear and groceries to their portfolio. To expedite this growth, it acquired six companies including Cult, Seraniti and Kristys in less than 4 years!

2018 to March 2020: The rise of Curefit

“We think of ourselves as, DNA-wise, like Apple. Very, very vertically integrated, that’s our core DNA”

– Mukesh Bansal

In the past two years, Curefit has emerged as the biggest brand in the growing fitness industry in India. The journey started with cult.fit by providing an end-to-end solution to India’s burgeoning fitness problem. Most of us get bored easily with gyms. So cult started with their own version of gyms where you work out in a group providing a sense of being part of a community or ‘cult’. A wide variety of workout forms and motivating trainers make retention rates for cult.fit much higher than regular gyms. It has around 500,000 active subscribers and is attracting more and more millennials. Despite growing competition from startups like HealthifyMe, Brilliant Wellness and Sarva, brand recall and deep pockets have enabled Curefit to stay ahead in the race.

There are six million active users in India who are spending an average of $350 to $400 annually towards fitness services, amounting to $2.6 billion market size.

– FICCI EY report

With 200 centers across the country, Cult contributes around 70% to Curefit’s revenues. Cult relies on an equipment light model compared to high equipment investments of traditional gyms due to which cult centers cost them 50% less to set up their physical centers. And they are just breaking even at the operational level on a month-on-month basis.

Eat.fit delivers healthy food through its app/website and other food delivery services like Swiggy and Zomato. It also comes with monthly meal subscriptions. Don’t confuse this with tiffin service. Eat.fit studies your exercise pattern and lifestyle and creates the perfect menu for the user. Not surprisingly, several of these users overlap across different offerings from their ecosystem.

While Cult.fit has a large ticket size, Eat.fit brings in about 80% of the users. In fact, its food sales grew by more than 10x from FY18 to FY19. It is serving about 35,000 meals per day, doubling every quarter.

Care.fit offers consultations, diagnostic tests and specialized services like skin, hair, dental and more. Along with Yoga and Meditation, Mind.fit provides psychotherapy sessions as well. While they have physical centers, their USP is that they facilitate an effortless digital connection between patient and doctor and give patients uninterrupted access to the prescriptions and medical records data.

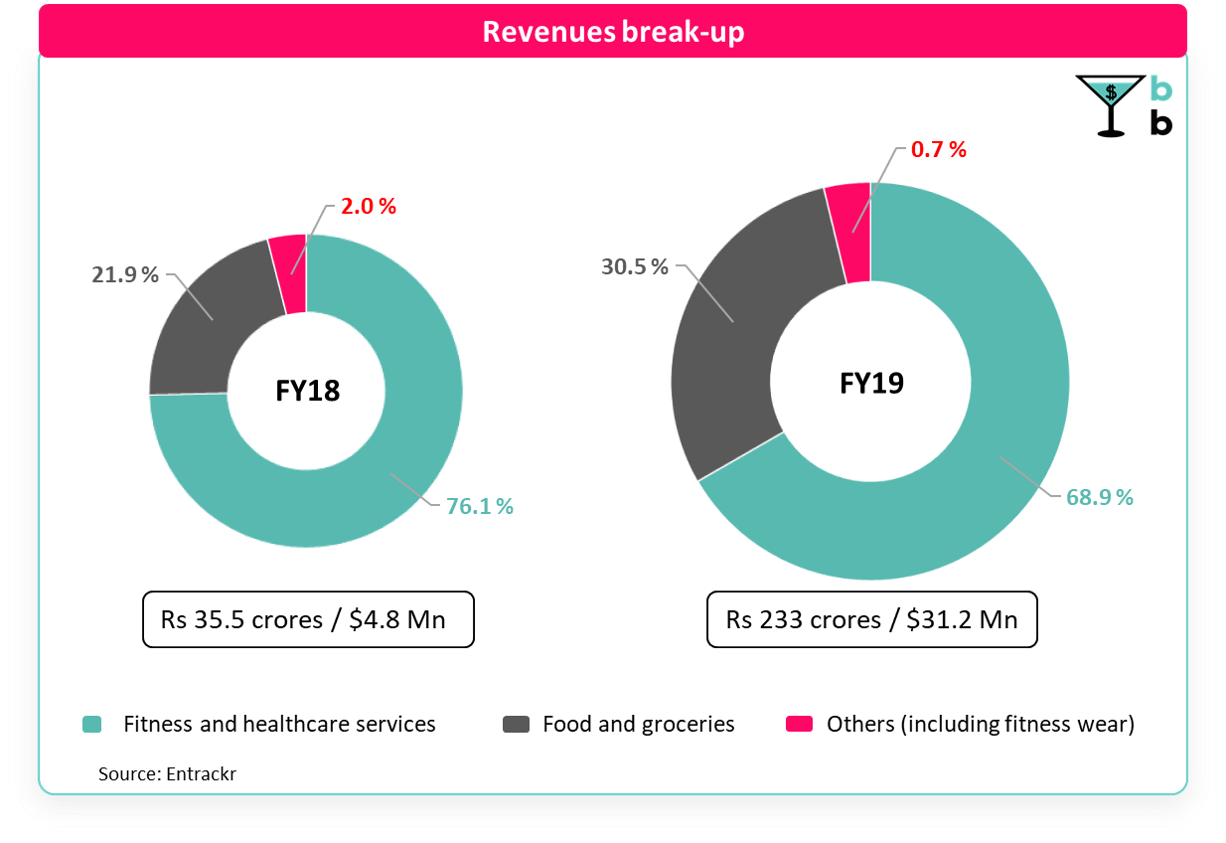

On a consolidated basis, the company’s total revenues grew 6.6x to Rs 233 crore ($31.2 Mn) in FY19 from Rs 35.5 crore ($4.8 Mn) in FY18. Like any other growth-stage company, this growth came at the cost of a huge cash burn. It spent Rs 5.3 to generate a single rupee of operating revenue in FY19, an improvement by 37% as compared to FY18 though. Total expenses ballooned to Rs 606.5 crore ($81.0 Mn) from Rs 130.9 crore ($17.5 Mn), year over year. Advertising promotional expenses, one of the largest brackets in the category increased fourfold to Rs 108.6 crore. As Curefit leverages network effects around its all-in-one fitness app ecosystem, the expense-earnings gap is expected to reduce further.

24th March 2020 – Present: The COVID Workout

Lockdown taken a heavy toll on the fitness industry. The total shutdown of the gyms forced companies to resort to salary cuts and furloughs. And Curefit is no exception to this. It permanently shuttered some of its small-town fitness centers. It also put as many as 18 cloud kitchens for sale. But even this couldn’t tame the beast.

All the gyms were shut due to lockdown, so it launched a wide variety of at-home digital fitness solutions ranging from personal training to live group sessions. It also partnered with Disney+ Hotstar to stream health and fitness content and gain access to Hotstar’s 300 million users. The newly launched segment is already getting traction and fitness enthusiasts who were regularly attending the fitness centers are happily shifting to the digital platform. More people have become health conscious now and Curefit’s cool features like energy meter for live sessions are luring tech-savvy young generation. Evidently, the virtual classes have grown with a million new users in the recent quarter, of which 80% were non-members.

With Eat.fit’s sales down to near zero during the lockdown, it is now pushing for groceries through recently launched Whole.fit division. Healthcare centers were also shut. And it is now eyeing to expand its foothold in the digital healthcare business. Beyond telemedicine, it also plans to expand into the preventive healthcare segment.

Curefit quickly responded with pivot and persist strategy and went all guns blazing. But will this really translate into a successful business? Let’s look at what lies ahead.

Post-COVID: Workout from Home

Prevailing pandemic has shifted consumer preference from physically attending traditional gyms to at-home fitness training. Based on the consumption data on Fitternity in the last 12 months, around 55% of the users opt for smart offerings in the new world of fitness. And the number is going to increase after the pandemic.

Curefit seems to be on the right track in capturing the digital fitness market, but the road does not look very smooth. Although the digital business will bring in more customers, the ticket size is relatively smaller. Compare the $400 annual gyms fees to that of at-home fitness sessions which ranges from $50 to $250 annually. Moreover, fewer capital requirements and low barriers to entry increase the competition in digital space. Companies like HealthifyMe, Fitternity, GoQii and gym chains like Gold’s Gym are already focusing on virtual training. Smart equipment and innovative products for at-home fitness offered by companies like Mirror and Peloton have been a big hit in the US and we will see such products flood the Indian market very soon.

We ran some numbers on our end and estimated Curefit’s 2023 market.

According to FICCI, the fitness industry will grow by more than double from $2.6 Bn to $6 Bn by 2023. Assuming the same growth for Curefit, the number of paying subscribers will increase to 1 Mn by 2023 across verticals. With high growth in its digital arm, Curefit expects 80% of the customers to access fitness services digitally in the coming years. At least 50% (of total) will be irregular customers who prefer to access the content at their preferable time from their home. Currently, this plan costs about $50 per user, which will bring $25 Mn in revenues (= 1M x 50% x $50). Rest 30% (of total) will come from people seeking live fitness sessions from personal trainers which currently costs $250. This will fetch around $75 Mn (=1M x 30% x $250). 20% will visit fitness centers and pay $400 annually, this will total up to $80 Mn (= 1M x 20% x $400). Adding the numbers gives $180 Mn in annual revenues by 2023. Still less than ⅓ rd of the current valuation!

Eat.fit may regain some traction in the future but given the attractiveness of the business, they won’t be alone. Already a business with thin margins, if any of the food delivery giants like Zomato or Swiggy enters the segment, it will give hard times to Eat.fit. Entering in Grocery business seems more of a distraction than expansion since this highly competitive segment will not do more good than eating away its cash.

India is leading in the adoption of digital health technology with 76% of healthcare professionals in the country already using digital health records (DHRs) in their practice. – Future Health Index (FHI) 2019 report

Prevailing pandemic has forced many hospitals, startups and companies to enter the digital healthcare business. With emerging technologies (like AI, big data, blockchain) and increasing internet penetration, India’s telemedicine industry is expected to create more than a $5.4 Bn market opportunity by 2025 with a CAGR of 31%. But numerous players ranging from startups to global companies like Dr.Lal PathLabs, Lybrate, Practo and Siemens already co-exist in stiff competition in the market. And Care.fit has a long way to go to compete with these already established players.

Curefit can leverage its deep-tech and strong on-ground network to lead in the fitness market. But it would be too optimistic to say that it will be successful in all its businesses with its highly complex structure (or ‘robust integration’ as they call it). It would do better to revisit the strategy and bring back some focus rather than just going crazy and losing it all.