Categories

Any discussion about cars, be it new cars or used cars, has to start with one man – Mr. Henry Ford!

In January 1914, one of the richest men in America was featured across major newspapers in the country – Henry Ford’s company was offering employees $5 an hour at a time when the average steelworker was paid about one-third of that wage. Ford, as we know it today, went on to build one of the largest automobile companies in the world. At a time, its factory had more than 100 miles of rail-road and steel & electricity plants of its own. The scale was so big that Ford even built planes for its government during wars, at the rate of one airplane per hour.

Ford wasn’t alone, America would have General Motors and its brands like Chevrolet and Cadillac and car manufacturers from Europe, Japan, and Scandinavian countries. The result? America was flooded with cars. Cars in America defined the common man’s lifestyle – what they drove, what they wore, where they ate. Cars were fashion accessories, used to attract the opposite sex and sometimes – determine where the common man had sex.

Car sales kept zooming all the way up until the 70’s – but then something interesting happened. New cars were no more seeing the explosive growth that they were used to. About 15.5 Million total cars were sold in the USA in 1978 – most of them fresh out of the box. The number of such new cars sold stands at about 17 Million for 2019. Figures for sales of cars in the USA have consolidated now for about 40 years. This massive influx of cars in the states then led to the creation of a new obvious category – Pre Owned Cars or Used Cars. Sales of used cars in the USA have gone from 36.9Mil in 2010 to 40.8Mil in 2019.

Up until Independence, India wasn’t really making cars. With Premier Auto and Hindustan Motors showing up after Independence, Padminis and Ambassadors filled the then small Indian automobile market. Later, Maruti Suzuki came into being, swooped in market share, and made the common man race to a new aspiration – a car – a Maruti 800. Maruti continues to dominate its presence with a 45% share in the market. Together with Hyundai at 17%, Tata at 8%, and Mahindra at 6%, these top companies have made the rest 17 players fight for the remaining 25% market. Similarly, Ashok Leyland and Tata Motors in commercial vehicles and Hero, Honda and TVS in two-wheelers account for 80% of the markets. Thus, revenues in automobile markets in India are pretty concentrated.

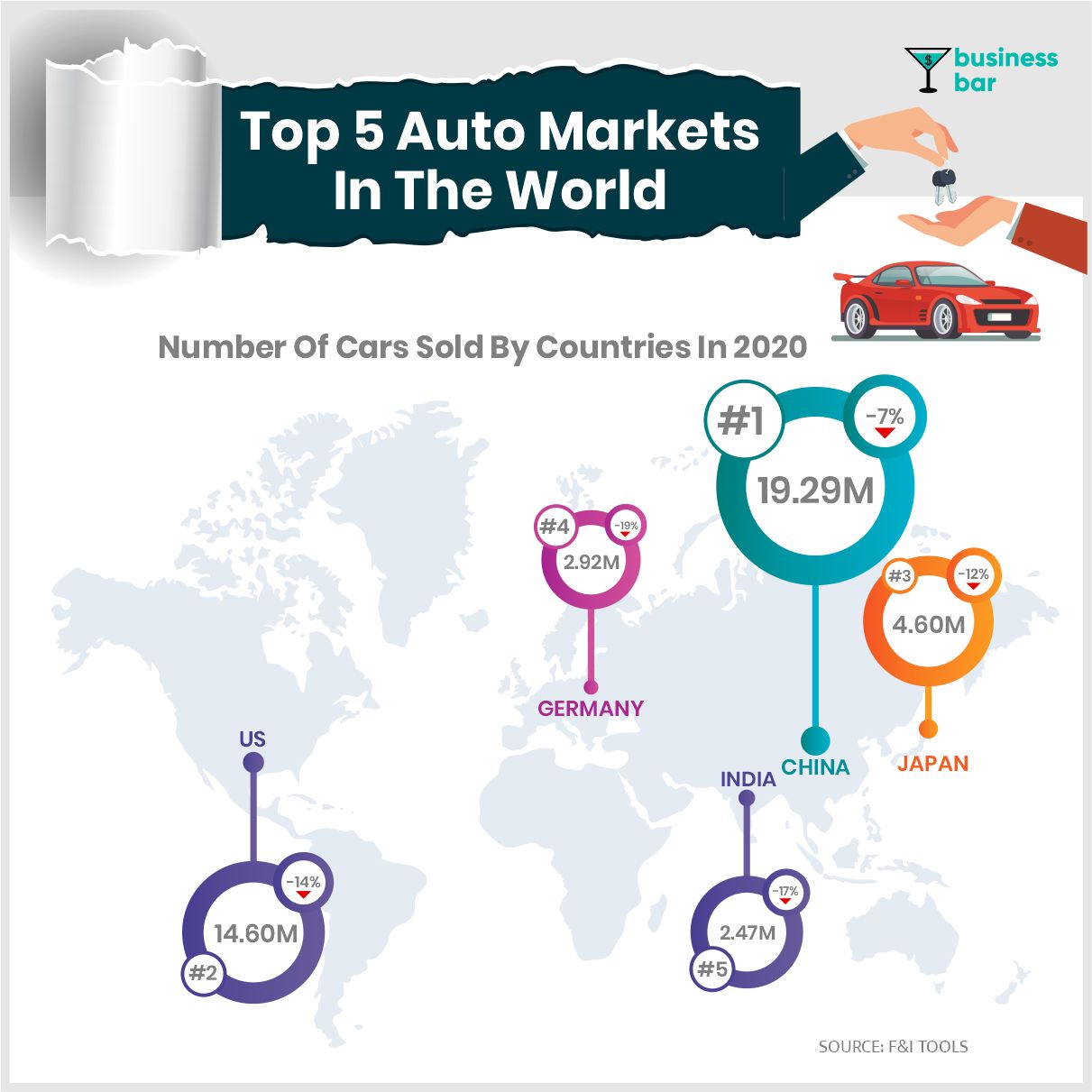

In 2017-18, India overtook Germany to become the fourth-largest auto market in the world behind China, US and Japan in order. Although it lost the No.4 spot later on the back slowdowns in the auto industry followed by pandemic induced lockdowns. As of 2020, the suppressed sales for the top 5 auto markets are shown in the infographic below, but for most trends and related analysis hereafter, we will resort to pre-covid data.

The sales of pre-owned passenger vehicles in India compared to newer ones is higher, but not as high as that in the other countries on the map above. In 2019, 4 million pre-owned cars were sold in India compared to 3.4 Million new cars – the ratio stood at about 1.2. It has been the same for 4 years since 2017. The same ratio, however, stands at 3.3x in the UK, at 2.8x for the USA and Germany, and at 2.5x for Japan.

The reason for developed countries having a higher ratio is two-fold. As we saw, in such countries cars have been a common possession for most families for decades now. By multiple sources, it is estimated that cars per capita ( #cars/1000 people) in the US is 20-50 times more than that of India.

In countries like the US, almost all new car sales are replacement demand and not the first purchase of an automobile in the family. While in developing countries, a lot of new cars are first ‘4-wheelers’ for the buyers. Implying that they don’t add to a unit on sale in the used-car market.

Secondly, people in ‘rich’ countries change their vehicles more frequently than those in the developing world. That is to say that a car in a developing country leaves the hands of the owner later than it would in a developed country. Thus, again causing a delay in the car making it to the pre-owned market.

So, one could argue – as India’s GDP per capita and urge towards self-mobility increases over time, there exists a big headroom for the pre-owned car sales market to grow. Another good news is that in this market which was valued at $24.24B in 2019, the majority of which is unorganized.

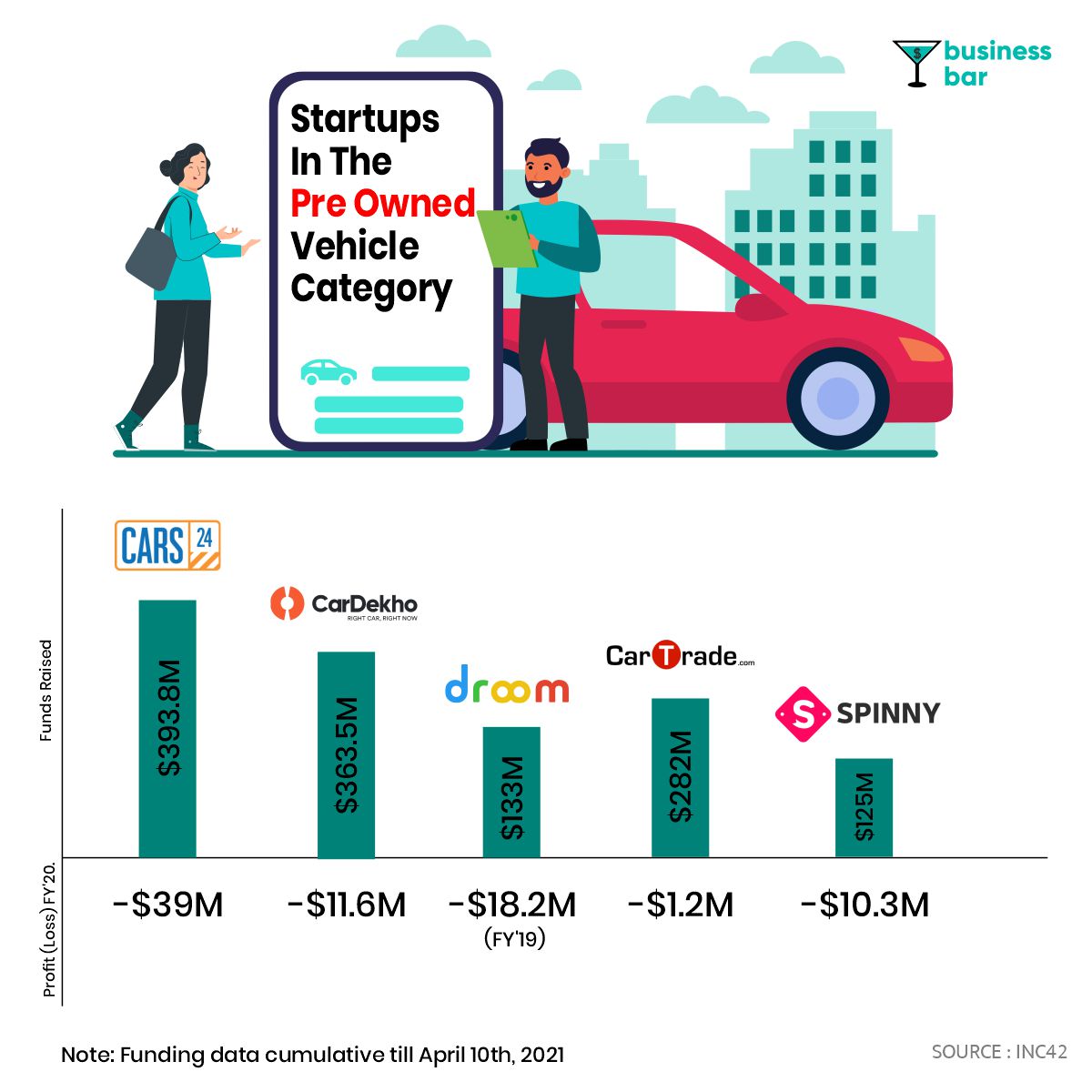

The majority of the Original Equipment Manufacturers (OEMs) already started organizing the used car market with brands like Mahindra First Choice (inc. 1997), Maruti True Value (inc. 2001), and what later followed suit are budding startups like CarDekho, Cars24, CarWale, CarTrade, Droom, Spinny and many more.

Mahindra First Choice and Maruti True Value lead the branded organized pre-owned car segment, selling 4.4 Lakh and 4 Lakh in FY19 respectively, expanding a hitherto unorganized industry. With the trusted brand name as a prefix in the name and source of funds on the balance sheet, both First Choice and True-value are tough competitors for the startups. On the other hand, the startups in the used cars industry have raised more than 1.2 Billion in total – each trying to solve the used car industry in their own way.

Additional services like credit for buying, insurance of the car, maintenance & repair, and others can contribute to margins and profitability – as much as 50%. It seems that a global pandemic was all these companies needed to spike their figures online.

But the entire business model does not have to depend totally on technology. Most of the bigger startups have gone the path of asset-heavy business models, with physical stores at multiple locations to serve customers and gain ‘trust’. Cars24 has stores in more than 100 locations across the country. Most companies in this space, be it in India or on a global scale, follow common practices. They visit potential sellers and perform standardized checks through trained technicians, prepare a holistic report about the condition of the car, and share the same with the buyers, ensuring as much transparency as possible.

Cars24

Founded in 2015, Cars24 went on to become the largest ‘startup’ in the used car space in India. It was estimated to sell around 200,000 cars a year and was able to double its revenue to over $430M in FY20, while expenses stood $39M more than revenues.

Cars24 operates in the C2C and C2B segments primarily. It employs an asset-heavy dealer model, that is to say, that they buy the used cars and then sell them to their ‘partners’ who further sell them to the end-user. That is why the whopping $430M number for revenues, had it been a marketplace model, a large portion of this number would have been called the GMV (Gross Merchandise Value).

To get into credit lending, it also applied for and was granted an NBFC license in 2019. Although profitability is still to be realized, the last funding round in November 2020, pumped in $200M into the company at a pre-money billion-dollar valuation, making it the first unicorn in the space. Earlier rounds of funding were also newsworthy owing to investors such as M.S. Dhoni and Sequoia.

CarDekho

CarDekho comes out as the No.2 among the used cars market startups as far as funds raised and valuations are considered. It surely is a ‘soon’icorn with a valuation reaching $650M in 2019, it will not be surprising if CarDekho joins the unicorn saga of 2021.

CarDekho tries to position itself as more of a holistic car classifieds portal and operates an asset-light model. With a revenue of $33.8M in FY20, it lost over $12M that fiscal.

Droom

Started in 2014 in Singapore by Sandeep Aggarwal, Droom is another company that sells pre-owned cars, scooters, bikes, planes and even golf carts and yachts. It claims it is contribution margin positive – meaning barring SG&A and R&D expenses, the company sees money on the books.

Functioning as a comprehensive online marketplace, its major revenue comes from the B2C segment and it. It claims to have crossed the $1B mark when it comes to GMV. In FY20, Droom did a business of $20M, but the expenses were nearly double at $38M.

CarTrade

CarTrade.com is an online car classifieds portal that has been able to attract investments of over $280M from funds such as Tiger Global and Temasek. Its revenue streams are multifold ranging from ad revenues to fees for relationship managers for car dealers. In FY20, they did $17M in revenues, posting a net loss of $1.2M.

Spinny

Founded in 2015, Spinny is another startup in the space backed by renowned angels such as Nandan Nilekani and has seen 4 major funding rounds, the latest being Series C in April 2021. It has raised around $125M to date.

It is a full stacked inventory based car-platform and boasts its high lead conversion ratio after the customer takes a test drive.

OLX

While OLX started as a product-agnostic marketplace for used items, it soon realized the potential in auto deals. Also at the same time, Luxury cars became another segment that has gained traction in the preowned category. The high rate of depreciation value of luxury cars, the fast-growing base of the young population, increasing disposable income of the consumers along side rapid urbanization have created a booming sub-segment. And OLX did not fail in capturing this opportunity, OLX reported to have an over 70% market share in the organized pre-owned luxury vehicles market.

As these relatively new enterprises try to tap into the unorganized markets, they look ahead to facing a lot of challenges and solving interesting problems on the way, aiming to make money and outperform the competition at the same time.

The case of used cars is a strong one from a buyer’s financial perspective. Buying used cars does not look like a bad decision. Statistically, new cars lose as much as one-third of their value within the first 2 years of use. Besides, stricter pollution standards rolling over every year make the costs of newer cars expensive every year. Compared to their previous versions, BS 6 petrol variants are estimated to cost Rs 10,000-50,000 more, while BS 6 diesel variants are estimated to cost Rs 50,000-1 lakh more. So, buying a pre-owned car definitely saves some money upfront. Besides, the insurance costs are cheaper, the car depreciates much more slowly and if you were to sell the car after using it for some time you could potentially get a little more money back.

Add to that the recent reduction in taxes to 12-18% on used car transactions from earlier 28% will serve as a nitro boost for the market.

On the selling end, the dealers have an incentive as dealer margins for a used car dealer are higher than those in the new car segments. In fact, the fixed dealer margin for new car dealers in most companies in India ranges between 3-5% while it is 8-10% for the US, 6-18% for the UK, 9-11% in China, and a high of 13-14% in many European countries. India stands lowest in the world. The highest margins offered are from Maruti and MG – a little over 5%.

There is a market for used cars and it seems to serve the sellers better margins, then what makes the road to sustainable profitability bumpy? Let’s look at the speed-breakers!

You see, the used cars business is a classic case of Lemon’s Problem in economics in which issues related to the valuation of an asset arise due to the presence of an information asymmetry between the buyer and the seller. The seller of the car, often, has the most information, and lack of trust is a major issue for the buyer that prevents opportunities for profitable exchanges. In the case-in-point for Lemon’s Problem, the buyer, thus, knowing he has lesser information would tend to pay a fixed base price and the seller- fully aware of this, would be inclined to sell lower quality ‘lemons’.

How do you fix this? Well, you bring a third-party marketplace – one that brings trust for the buyer through transparency and essentially, removes the information asymmetry. And so, you get Orange Book Value, Indian Blue Book and various other car-quality reports used by these startups, each trying to convince its customers with quality assurance and beat competitors at price discovery at the same time. The USA follows a standard Kelly Blue Book pricing for used cars – which is generally accepted by both consumers and the automotive industry in the US.

The challenges for the players in pre-owned car sales, unfortunately, do not end at the trust. Price is the second major consideration after quality conditions that users have in mind while buying or selling a used car. Hence, all the players would want to beat competitors at price discovery. At the end of the day, these startups are businesses after all, and so ensuring profitability while providing the best price to the customers is the third major challenge. In the US, firms like Sonic and CarMax base their marketing around the fact that they don’t haggle. The price you see is what you pay. Ensuring trust, price discovery, and profitability all at the same time makes the used-car business a tough nut to crack.

Another incoming trouble seems to come from the electric vehicle revolution. With rising in EVs and the new millennial buyers’ conscious shopping behavior EVs pose a threat to the used car dealers until the few years before EVs start becoming ‘2nd hand’.

In any country, the automobile industry is 8% to 12% of GDP and the largest or among the top 3 retail categories. However, unlike travel, mobile phones, electronics, fashion, food, or jobs, automobiles have low online penetration. And rightly so, startups in this industry realized that a used car marketplace is more of an offline to online business than a pure-play technology business – online classifieds never sold cars really. Smooth customer experience while buying/selling an automobile is a priority for all startups. On Cars24 for instance, one can sell a car and get money in the bank within as quickly as a day.

Startups in the space are still trying to convince themselves on what business model is the best! For instance, the situation with the used cars industry is similar to the one faced in the hyperlocal industry – do you as Cars24 (BigBasket) keep the physical stores (warehouses) and maintain them or use merchant delivery channels like CarDekho (Dunzo) and stay asset-light. Who is correct with the problem at hand? Be it used cars or grocery – only time will tell us.

But most players have seen a recovery to pre-covid levels in light of tailwinds such as GST reduction, urge for self-mobility but in the startup world, they say, you need to run to remain where you are, to get ahead, run faster! So how are these companies trying to shift gears up?

According to Cars24 CEO Vikram Chopra, most of the emerging players are targeting data. Data could really be the oil for these internet companies, knowing your credit history and your car’s condition is a gateway to all the additional services we can offer.

“The cars we drive say a lot about us.”- Alexandra Paul

And who knows, soon the cars might not just be a social statement but actually be telling a lot about us. We believe that newer ‘internet cars’ such as those by MG and Kia in India can help solve the car data collection problem, but getting hands-on such data will still be a challenge for the startups in question. Other startups like Park+ and Get My Parking serving the smart-parking segment can be the potential sources of data here, and hence it’ll not be surprising to see if players in the used cars business go after acquiring such startups as long as their newly propped up hunger for user data gets satisfied.

This article was co-contributed by Skand Gupta.