Categories

The origin story of beer is a fascinating one, and a lot older than you think. Beer is perhaps the oldest fermented beverage known to mankind with some of its earliest records dating back to 2000 BC! In the early days, water purification wasn’t as sophisticated as it is today. The only way to purify water was to boil it. Then people started to add certain herbs and spices to give the water antimicrobial properties and extend its shelf-life. But they made the water taste bitter. So, people added malted cereal grains to give it a bit of sugary sweetness from glucose. This bittersweet concoction was stored in large vats where yeast took hold and began the process of fermentation. That, my friends, was the first instance of a beer. You could technically say that in a way, people did save water by drinking beer, eh?

In today’s special, let’s look at what is brewing in the beer business across the globe and within the Indian beer market, which houses one of the world’s largest beer-consuming populations.

Beer is the largest segment of the alcoholic beverage market which is valued at ~$1165B. Out of which the global market for this beautiful concoction is valued at a whopping $651 billion and is expected to continue its upward trajectory at a CAGR of 7.42% (2021-2025). The United States continues to remain the single largest market by revenue, forecasted to generate over $112 billion in 2021, followed by Europe and Asia-Pacific. In terms of consumption, China held the top spot with ~21% of the total market share by volume. The US is the 2nd largest (~12%) consumer (although consumption declined by 0.5% last year).

The whole industry is quite consolidated and continues to get more so as a result of a plethora of acquisitions by top players. The industry is characterized by high barriers to entry created by high fixed costs, restrictions on advertising, well-established global distribution networks of incumbents and strong brand identities of existing brands.

There are 4 key players in the global arena, which make up over 51% of the entire market, including ABInBev, Heineken, China Resource Enterprises and Carlsberg.

ABInBev alone holds the dominant share of 26.2% with iconic brands like Budweiser, Corona Extra, Haywards 5000, Stella Artois and Hoegaarden in its portfolio. Curiously, the company’s strange name was a result of a series of mergers and acquisitions of various long-standing breweries from across the globe. Interbrew, Ambev and Anheuser-Busch merged in the early 2000s to create the ABInBev umbrella under which many other breweries came together such as Mexico’s Grupo Modelo and South Korea’s Oriental Brewery and SABMiller. With annual sales exceeding a mind-boggling $50 billion in 2019, thanks to its flagship Budweiser it seems unlikely that any company can come close to dethroning it.

Heineken has held steady at the second position in terms of overall global market share of 11.5%. However, in the premium beer segment the company holds the lead through its flagship brand, ‘Heineken’. The company also counts among its portfolio over 250 international, regional and local brands such as Coors Light, Fosters, Birra Moretti, Sol, Strongbow, Desperados etc. Heiniken did ~$27B revenues in 2019.

While ABInBev and Heineken may hold strong overall market share, the single top selling beer brand is Snow, owned by China Resources Enterprise Ltd, which retails for just $1 per litre (33 cents a pint) in China. This is outrageously cheap and well below the average price (Supermarket and Restaurants) of a pint in China ($7.71), the US($4.75), the UK ($5.97) or even India ($3.90).

The most expensive beer in the world is found in Dubai, where an average pint can easily run you $12.

China Resources Enterprise operates as a holding company and has its footprint across food and beverage retail in rice, fruits, vegetables, meat and beer. However, beer accounts for 51% of its total business and the company holds a 6.6% market share in the global market. While many of us may not have heard of the company, its iron grip on the Chinese beer market is enough to grant it a revered position among global players. In fact, just last year, Heinken acquired a 40% stake in the company in order to expand its reach within this billion people plus Chinese market.

Carlsberg may be 4th on this list, but it still is a formidable contender in the global beer market. The company controls 5.9% of the global beer pie with iconic brands such as its flagship Carlsberg along with sub-brands like Carlsberg Elephant, Kronenbourg and Brooklyn Lager.

Per capita wise, Czech Republic consumes most beer in the world with 143 liters per year, followed by Namibia (108 Litres), Austria and Germany (~106 litres)

India gets its high from whisky, and Beer is the second most popular alcoholic beverage in India.

India consumes more whiskey than any other country in the world and most revenue is generated in India ~$21B

India Beer market size amounts to ~$15B and is expected to grow annually by 10.14% (CAGR 2021-2025).

While the global market is dominated by ABInBev, in India, the company is relegated to the second position in terms of market share. The dominant player in this market is the owner of the ever so popular ‘Kingfisher’, United Breweries Ltd. Although ABInBev still commands a 65% share of the premium beer segment in India. In fact, the overall Indian beer market is even more consolidated than the global one with the top four players, United Breweries (51%), ABInBev (20%), Carlsberg (15%) and Mohan Meakin (~2%), controlling about 88% of total sales volume. While Heineken’s absence in this league table is quite a surprise, the company does have skin in the game after its acquisition of Scottish & NewCastle plc, which held a 37.5% share in United Breweries Ltd. In India, Heineken and its associated brands are sold exclusively by United Breweries Ltd.

ABInBev and Carlsberg have secured their respective positions in 2nd and 3rd place in terms of market share on the back of their widely popular flagship brands Budweiser and Carlsberg respectively. In addition, the Indian population’s affinity for stronger beers has made the companies’ sub-brands, Budweiser Magnum and Carlsberg Elephant, with their stronger ABV%, big favourites in the country.

While Mohan Meakin may be more closely associated with one of the most recognisable rum brands in India, Old Monk, the company also manufactures beer under various labels – Golden Eagle Lager, Gymkhana Premium Lager, Solan No. 1 Premium Beer, Old Monk Super Strong, etc. Its beer does not hold a candle to popular brands like Kingfisher, Budweiser and Carlsberg in metro cities. However, in some tier 2 and 3 cities, the company’s beer brands sell exceedingly well.

Although the majority of market share is controlled by above mentioned industrial/mass-produced beers, a new wave of craft beer revolution is coming up in the Indian booze economy. Globally, Craft beer is usually found to be a premium tier drink, appealing to urban “hipsters” in large markets.

Unlike beers produced at large scale, these craft brews are created in small batches using specially curated recipes, not formulas. Hence the term ‘craft’.

For a very long time, centuries even, the Indian population was sufficiently satiated with strong golden brown lagers mass-produced by the aforementioned global players. However, the introduction of craft beer in the past decade opened up a whole new sub-sector at the premium end of the beer market. By 2019, the craft beer market expanded to over 43 million liters by volume: an exponential rise from just 0.15 million liters in 2014.

Craft beer is known for its authentic, non-mechanized manner of production which allows for significant experimentation opportunities with flavors. In India, over the past decade, brewers have built up exceedingly unique beer-drinking experiences by leveraging local ingredients such as coffee, honey, cardamom, cloves, ginger, saffron, among others.

Innovative craft beer start-ups like Bira, White Owl, Witlinger and microbreweries like Doolally, Toit introduced the Indian audience to several unique flavors and have captured a portion of this premium market.

But the sector is still nascent. 90% of the overall beer market is dominated by mass-market beer brands such as Kingfisher/Tuborg and 10% is controlled by premium brands such as Budweiser and now, craft beer brands like Bira. Of this, craft beer accounts for less than 2%. And within that 2% craft, there is a huge competition and making money, thus, becomes an uphill task. But that isn’t deterring Craft beer’s rising volumes.

Ayush Bagla, who looks after finance and strategy at White Owl, told us, “Given the fact that craft beer is made using natural ingredients and no adjuncts that also make it relatively quickly perishable, along with the economies of scale that favor large breweries to a great deal, craft beer is priced at a premium to mass beer. But craft beer is more of an experiential thing and with more people trying out crafts and developing a taste for craft and its quality, customers are getting comfortable in paying a slight premium for good quality beer.”

Unlike other FMCG industries, pricing and competition are not the biggest challenges because the alcohol market is heavily at the mercy of the government. “In India, you don’t have a single market, you have 28 markets, each state with its own regulatory challenges. Somewhere it’s the distributor-driven market, while in southern states you’ll find corporations or a more stringent tender-driven market such as in Kerala and Telangana. In states like Haryana, the concept of MRP doesn’t exist and they are allowing the market to price the product freely.”, Ayush added.

Bottled craft beer pioneer Bira which sells Bira Blonde and Bira White, counts Sequoia Capital and Sofina among its earliest backers and has raised over $160 million to date with its most recent round of $30 million coming from Japanese beer maker, Kirin Holdings at ~$300M valuation. When they entered in 2015, there was close to no competition in this space.

Now, there are more than 45 brands (such as Chhattisgarh-based Simba, Mumbai-based White Owl and Gurugram-based White Rhino) in the same premium price range as Bira — Rs 100-150 for a 330 ml bottle. All of these in just the past 5 years. In the face of so much competition, Bira doubled its losses to ~200 Cr in FY19 as compared to 2018 and revenues stood at ~183 crore which is just a mild growth of 15% as compared to 158cr in FY18.

Microbrewery business serving craft beers on tap at the brewing location itself is also catching up in India. Doolally was India’s first microbrewery, founded by IIM Bangalore alumnus Suketu Talekar. It was set up in Pune, Maharashtra as it was the only state to grant a microbrewery license back in 2009. Even today, only a handful of states provide a microbrewery license: Karnataka, Haryana, Punjab and West Bengal.

As per Ayush from White Owl, “We expect the number of microbreweries and new beer brands to rise in India, but these will help the category and consumers to evolve. Bars & Restaurants form less than 20% of our sales split, and it even reduced to less than 10% post-COVID’s initial lockdowns. These newer brands will increase the pie rather than taking a share of the pie.”

Most Recently, dominant players like United Breweries and ABInBev have also taken an interest in the craft beer market. United Breweries launched the Kingfisher Ultra Witbier at a price point in direct competition with the dominant brand in the segment, Bira White. ABInBev partnered with the Indian Hotels Company Ltd., owners of the Taj brand, to set up a chain of 15 microbreweries over the next 5 years.

There seems to be a lot of tailwinds for the craft beer industry, the volumes are also rising commendably, but are still not big enough to make these startups sustainably profitable yet.

Well, here comes COVID-19. As India entered into a complete lockdown in March 2020, the alcoholic beverage industry came to a standstill. Alcohol was obviously part of ‘non-essential’ businesses so all of its sales across channels were halted. In fact, this led to a surge in internet searches for methods to procure alcohol across the country. The beer industry suffered a greater deal as beer is a lot more perishable compared to stronger liquors.

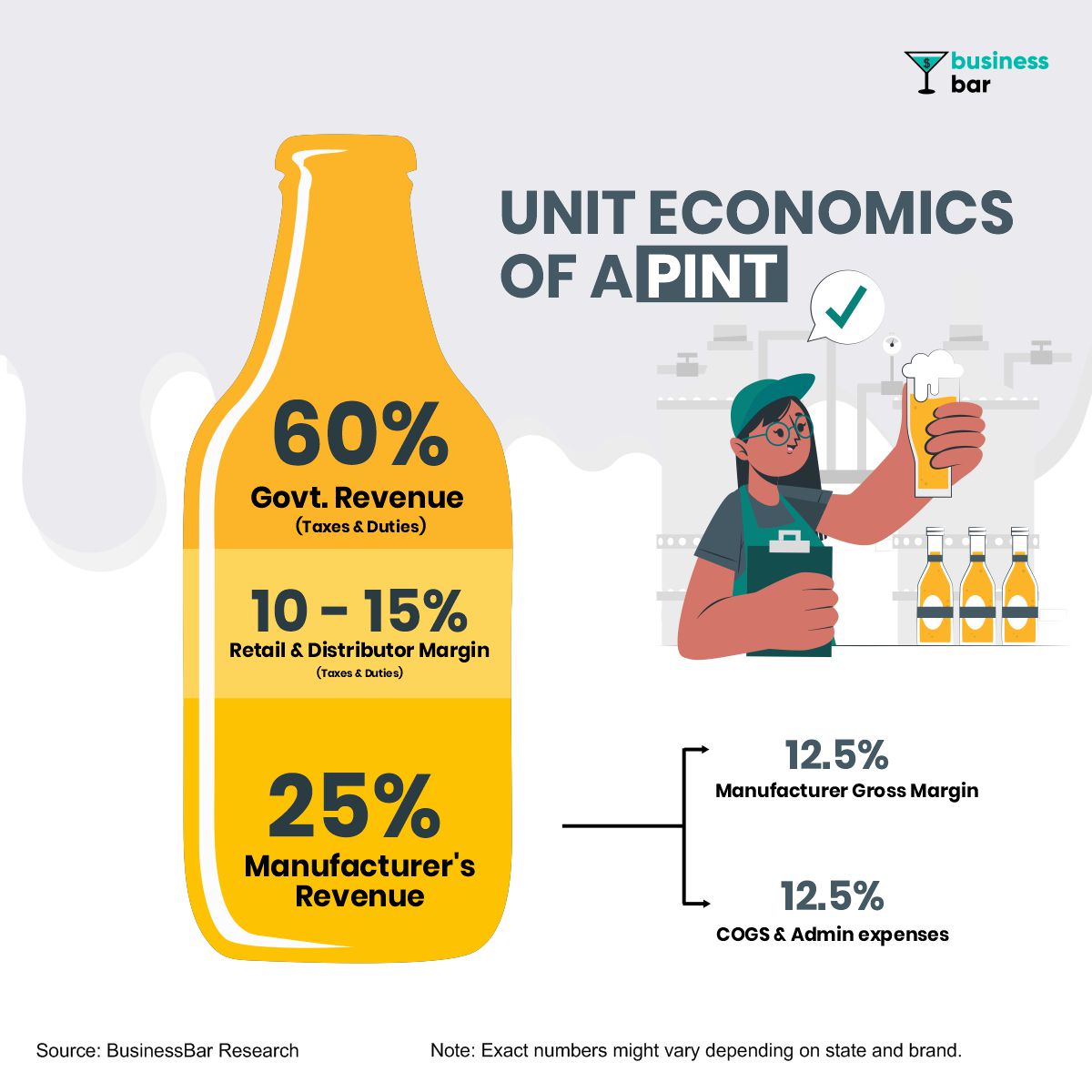

It was only in the third phase of the lockdown when alcohol sales were permitted. Although, this was coupled with a price hike in the form of a new COVID cess. ranging between 10 and 75%. Again, beer was disproportionately impacted as it is already taxed 60% higher than stronger spirits.

Alcohol in India is taxed on volume rather than alcoholic content. A litre of whiskey would attract the same tax as a litre of beer

A nationwide ban on alcohol sales during lockdown caused a revenue loss of ~$6B. And the government lost a big chunk of tax collection. To put it in perspective, tax from alcohol sales contributes ~25% to the state’s revenue. So, India was finally ready to have a conversation on the delivery of liquor. Certain states and regions like Maharashtra, West Bengal, Bengaluru, Jharkhand, Odisha permitted home delivery of alcohol. This led to several breweries setting up online storefronts for their growlers (pressurised containers directly filled from microbrewery taps) along with alcohol retailers such as LivingLiquidz, HipBar selling online through websites and even via WhatsApp. Moreover, the online delivery option gave rise to ancillary businesses like beer subscription services – Buzzed.in in Bengaluru and TappedFlight in Mumbai.

Seeing a lucrative opportunity, several companies started hyperlocal delivery in 2020. Swiggy, Zomato, Amazon, Big Basket started alcohol delivery in some states. Modern Trade outlets like Spencer’s got an incredible opportunity to push their omni-channel strategy (both offline stores+online). However, the question around scalability and profitability still remains as there are numerous restrictions and regulatory hurdles. Zomato has in fact exited the alcohol delivery business and is concentrating on food before its IPO.

With recent disruptions in the beer market due to COVID, United Breweries expects further acquisitions and new entrants in the coming years. India is going through an incredible journey – higher disposable incomes and gradual social acceptance of beer as a casual drink. Larger players may continue acquiring up-and-coming craft breweries to further strengthen their foothold in this premium end of the beer market.

There has been some regulatory support as well. The Haryana Excise Department revealed a new alcohol policy that provided a separate classification for beer & wine and reduced taxes on the same. An additional category of ‘super mild beer’ having very low alcohol content has been introduced which enjoys lower excise duty. If these regulations do find popular appeal among other states in the country, the beer industry will grow at a much faster rate than the rest of the world.

At the global level, top players will also continue to focus on high-end event sponsorships like the Premier League, Formula One, SuperBowl etc., and innovative marketing campaigns to build and maintain a differentiated identity.

In the long term, the industry faces a major threat from legalisation of cannabis around the world. Marijuana is seen as a substitute that can eat up the industry revenues with a major overlap in the customer base. Well what do you do in such a case? You diversify. This is exactly what Anheuser-Bosch has done with a joint-venture with Canadian cannabis producer Tilray. Well, this threat also poses a unique opportunity to diversify into products posing a threat of substitution to beer in the future such as hard seltzers, alcoholic kombucha and CBD & THC infused beverages.

Whatever happens, the age old players will still remain competitive owing to their substantial capacity to for mergers and acquisitions. Moreover, in order to stay innovative, many companies in this space also fund and develop accelerator programs for “moonshot” ideas in the industry like new products, innovative distribution platforms, etc.

All in all, there’s a lot brewing in this ancient industry.

Cheers 🍻

This article was co-contributed by Abhishek KulkarniWe thank Ayush Bagla, Executive – Finance, White Owl, for sharing his insights with BusinessBar.

1 comment