Categories

“Everyone, deep in their hearts, is waiting for the end of the world to come.” – Haruki Murakami, 1Q84

You might also recognize the above quote from the movie ‘The Big Short’, displayed right before they show the collapse of the financial system and the subsequent crisis in ‘08. The point being, that crises are no new thing as far as the history of industries and businesses is considered. In fact, the cycle of boom and bust, of expansion and contraction is a well documented and well understood (but not well anticipated) phenomenon.

What distinguishes the COVID crisis from the rest is its modus operandi. Locking down about half of the earth’s population (way more than half if their output is considered) has brought economic activity to levels of unthinkable lows (be it the demand or the supply side) in incomprehensible spans of time.

The impact and its tremors are being felt in almost all traditional sectors of the economy, but some are hit more than the others. Disruptions in the travel industry are pretty evident, the pressure that airlines around the globe (no pun intended) are facing has brought them to ask the governments to help them avoid crash landings (pun intended).

You can read our piece on what lies ahead for the airlines here at Airlines – The pursuit of happiness.

But companies who ‘fly’ planes aren’t the only ones who are worried, there’s one more sector that is being haunted by the shockwaves of the COVID crisis – the companies that ‘make’ planes.

Let us take you on a tour of how the ‘aircraft manufacturing industry’ has evolved over the decades, navigating its way through problems that range from aircraft safety in the sky to geopolitics on the land.

You must be familiar with names like Boeing, Airbus, and… and… and none?

If you also couldn’t get a third name in your mind don’t worry, it’s probably not your fault. It has been this way for quite some time now – a hell of a duopoly. Let’s take off to see…

Both Boeing and Airbus, each control about 50% of the large commercial aircrafts market. Yes, you read that right, together they control over 99% of large commercial aircraft deliveries worldwide.

For most flyers, both the companies and their products are invariably the same. For those who buy from them, the reasons are often not product-related as pilots around the world have said that planes from both manufacturers in the same segment are more or less the same standard. Boeing, founded in the US in 1916, has always been a big player since it has been here since the dawn of aviation. On the other hand, Airbus has had a bumpy ride. It started in the late 60s in Europe as a joint effort by some countries to take on the manufacturers on the other side of the Atlantic. Airbus has then seen merger after merger across Europe which has given rise to what is now called the Airbus SE Corporation, the European consortium with headquarters in the beautiful dutch city Leiden and operating head office in Toulouse, France.

Both companies deliver 800-900 aircrafts every year now and have backlogs of thousands of deliveries on account of the made to order nature of the business.

Boeing and Airbus together brought in north of $172Bn in revenue and more than $16Bn in net income in the year 2018.

Barriers to entry in the industry are simply huge, be it the massive capital requirements (new program costs ~$20Bn) or the colossal know-how requirements (well yes, it is some kind of rocket science). That explains why no new players have emerged in the sector. Has it always been this way? Just Boeing and Airbus. No, not really.

Both Boeing and Airbus rule the skies when it comes to large commercial aircrafts, but when it comes to small regional jets, the Canadian company Bombardier and the Brazil-based jet maker Embraer have been the top guns for long (and until very recently).

Now do we have two duopolies?

For the moment, yes. Let’s find out how long this will last.

In 2016, Bombardier received an order for 75 of its new C-series jets from US-based Delta Airlines. This was seen as a dent to the Boeing-Airbus duopoly. Boeing, with the help of its friendly ties with the White House (read successful lobbying efforts worth hundreds of millions of dollars), managed to get deal-breaking tariffs imposed on the transaction. The Quebec based manufacturer Bombardier did not have the financial muscle to battle its way out of this. Airbus came to the rescue and took over the entire C-series program. Bombardier was pushed into a corner and the deal included Airbus acquiring 51% of Bombardier’s C-series program for, wait for it, just $1. It was so because this got the 300% import tariffs waived off as Airbus could make the planes in the States itself.

This gave Airbus an entirely new segment of passenger planes in its offering while also practically killing Bombardier and the threat it posed. Boeing, in apprehension, did the only thing it could do in its defense. It announced to buy 80% of the only remaining ‘real’ competition to the duopoly, Embraer’s commercial division, for 4.2Bn dollars in 2018. This was seen as the final nail in the consolidation of the industry. But as recently as in April 2020, the Boeing-Embraer deal is said to have collapsed, although this equally severs the purpose looking at how desperately Embraer wants a deal to occur.

The competition from the rivals of the US, the old and the new, Russia and China, has always been substandard. It has been broadly because of the approach they’ve been employing – running a government operation to meet commercial needs and secondly, relying on stuff made in the home country itself, limiting access to state of the art global intellectual expertise. Though China’s state-run manufacturer COMAC may turn out to be a real player on the back of strong domestic demand anticipated in the future. But for now, it is safe to say that this competition is decades behind.

Just as the automobile sector is positioned to be won by those who win the battle for electric cars, you may wonder what about Electric Planes! After all, that’s some pretty serious carbon footprint reduction in sight!

The short answer is, it is not a question of when we will have electric planes but a question of when we will have batteries that will let us fly to distances as far as those that plane do have to traverse.

As far as supersonic jets are considered, there are a few barriers it has to overcome before it becomes commercially viable (and sound barrier is definitely not one of them). The loud noise, pollution, high costs (5x the costs for 2x the speed), and a few mishaps with the Concorde program in the past have made supersonic jets illegal pretty much everywhere worldwide.

Thus for now it would not be an overstatement to say that what we have is a ‘super duopoly’.

But with great power comes great responsibility. Safety is an utmost priority when it comes to flying. And it should be a matter of pride for the human race collectively that we have reached the levels where 4 billion passengers fly in a year and less than 500 of them are involved in crashes or in some years, even zero. This has been achieved by taking each flying mishap under great scrutiny and after the two crashes last year that claimed more than 300 lives (Lion Air flight 610 and Ethiopian Airlines 302), the immensely popular bestseller Boeing 737 Max 8 were grounded by the regulators worldwide. It was a major blow to both the budget airlines and Boeing. Airbus on the other hand had been involved in regulatory fists and bribery investigations in both the USA and Europe. It agreed to wrongdoings and paid around $4bn in fines.

Then entered the coronavirus, earlier when the order books of both Boeing and Airbus were brimming, customers complained about the long lead times. But the massive decline in passenger demand has rendered part of the existing airline fleets idle, forget about adding new planes.

Out of the 24,000 commercial planes in operation worldwide, around 16,000 or two-thirds were grounded during the coronavirus lockdown measures.

When airlines around the world are on the verge of filing for bankruptcy protection, it is a no brainer that even the existing in-pipeline orders will suffer, be it deferrals in deliveries or straight up cancellations. Q1 2020 saw orders for 196 and 66 jets being canceled for Boeing and Airbus respectively. They also laid off up to 10% of their total workforce (both employ about ~300,000 employees combined) and furloughed other tens of thousands of employees. No wonder the stocks of both companies have seen a fall of over 60% this year.

The financial results for the six months of H1-2020 released recently are a testimony to the weak demand. As expected, both reported losses. Revenues dropped by 26% and 39% for Boeing and Airbus respectively. Deliveries were down from 239 to just 70 for Boeing and Airbus delivered just 189 planes in the six months compared to 389 in same period last year.

There’s no doubt that the skies ahead are full of headwinds for both the behemoths – Boeing and Airbus, but they say, there’s always a silver lining in every cloud.

Both Boeing and Airbus are not only giants in the commercial aviation manufacturing industry but also employ their ability to put together thousands of parts that work in symphony, in a fashion where the margins of error are minuscule at best, to manufacture military aircraft, weapons systems, strategic defense and intelligence systems, and related products and services.

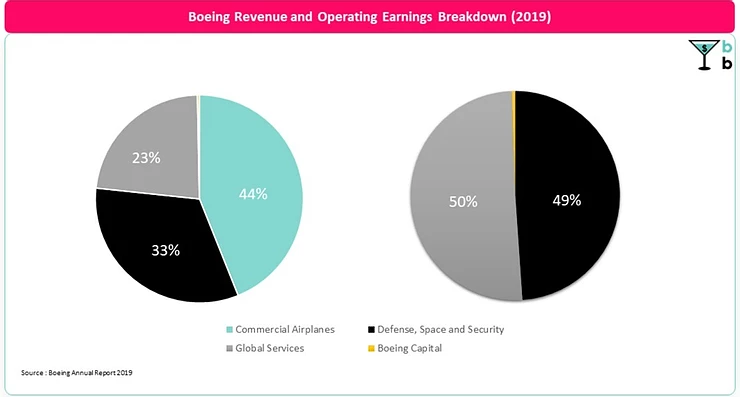

Boeing has had the honor of securing the lion’s share of the US Department of Defence’s procurement budget, second only to the world’s biggest defense contractor Lockheed Martin. The White House has been the biggest customer of Boeing accounting for 39% of the total revenue that it brought in 2019.

Of the $75Bn dollars that Airbus boasted as its topline in 2017, 21% came from Airbus Defence and Space – the namely self-explanatory subsidiary of the Airbus SE corporation. About 10% of Airbus’s revenues come from its helicopter division whose market is expected to be stable if not in an uptrend in the near and middle term.

Thus even with commercial aircrafts being the biggest dollar bringers for both companies, it is noteworthy that about a third of the sales come from the Defense, Space, and Security related divisions. How crucial these divisions may prove can be seen below by the fact that this third of the revenue funneled down to around half of the operating profits for Boing after the 737 Max fiasco.

Boeing has even received a $1.5Bn contract from the U.S. Navy amidst the pandemic.

The coronavirus has taken over as the center point of discussions globally, but allow us to remind you that 2020 hasn’t been a kind year geopolitically either. The US-Middle Eastern tensions that intensified in early January when Trump ordered the killing of a prominent Iranian General in Bagdad made the media outlets feel as if it’s 2004 again in the region, if not the precursory action for WWIII. Yemen has been going through one of the worst humanitarian crises in history where the US made Saudi imported warfare machines like missiles made by Boeing are at great display.

As if the India-Pakistan Airstrike tensions last year weren’t enough, China has triggered conflict at its frontiers on the Indian side. But China has seen tensions rise with almost every other country be it their frenemy theUS or allies like Russia. Arguably the world’s most tense border – the DMZ that dissects the Korean Peninsula has seen some turmoil as the DPRK announced to cut all ties with Seoul. Not to forget that globally militant activity and the war on drugs and terrorism already has been a place where governments have been spending billions of dollars of their defense budgets, every year. Before we start sounding cynical if we haven’t already started to, the point is that as per the status quo, spending on ‘Defence and related activities’ is only going to go up in the name of ‘world peace’. And that should be good news at least for the two companies we have been talking about.

While Boeing has had an upper hand in the Defence and Security division, its 737 Max troubles and the recent fallout of Boeing-Embraer deal will give an edge to Airbus to capitalize on the commercial business recovery, sooner or later, as it happens. Both the companies are ‘too big to fail’ or indispensable even in such turbulent industry dynamics. The longer the pandemic lasts, the degree of structural changes might increase but if you were to buy a plane after the pandemic, it’d likely be made by either of the two. Meanwhile, the strategy in our opinion should be to attain a hybrid revenue mix while they search for the next breakthrough product (or service!).

Hence, if the popular question from the animal kingdom in response to a crisis – ‘Flight or Fight?’ was to be asked to Boeing and Airbus now, the ideal answer should be – ‘Both, Flight and Fight!’.

1 comment