Categories

Digital Lending has taken over the majority of all chatter around startups over the last few months. Owed in part to its growth, and the attention it attracts from the RBI. Although Digital Lending encompasses lots of different models like personal loans and all digitally approved loans, in this edition of BusinessBar, we are going to discuss the fast growing Buy Now, Pay Later – a lending solution offered at the point of sale, or rather the checkout if we strictly talk about digital BNPL.

BNPL lies at the intersection of 2 giant industries – ecommerce and lending. The BNPL market is currently at $3 billion and expected to be worth $45 billion by 2026, according to a study by Goldman Sachs. That means growing at 73% annually – contributed by the rising ecommerce market and the increased adoption of BNPL as a payment method.

Covid-19 pandemic boosted online retail at the cost of offline sales. Online now accounts for 6.5% of the Indian retail market compared to pre-covid levels of roughly 3%. But, BNPL took off massively on ecommerce when Slice entered the game.

Slice was issuing almost as many credit card challengers a month as top banks like HDFC and ICICI. For context, Slice acquired 12 million customers in just 3 years of operating when the total credit card base is just 60 million Indians. That’s a serious challenger.

What makes BNPL different from other digital lending solutions like Payday loans like EarlySalary and personal digital loans like Navi, Dhani, MoneyTap and the likes?

It’s in who’s paying for it.

BNPL – Buy Now, Pay Later. It’s in the name. It enables a consumer to buy what they want (and sometimes don’t) and not worry about paying it now. From a business point of view, BNPL is then more about commerce enablement than it is about lending. Of course technically a loan is being given out, but it is used for a specific purpose.

The BNPL payment method boosts avg order values and conversion rates for merchants. And because of this the merchants who sell via BNPL can afford to pay higher commissions because they sell more and earn more. (The commission a merchant pays to the payment provider is usually called MDR or Merchant Discount Rate). Simpl, for instance, advertises 20% higher AoV and 2x the order rate to its merchants. This is why the MDR for the BNPL payment options is close to the credit card MDR of 2% compared to 0.5% for debit cards and 1% for wallets.

Merchants like BNPL because it increases their revenue even if it comes with slightly higher commissions. All the more reason why BNPLs spend huge money on acquiring customers. There is an opportunity to earn around 24% p.a return on your capital (2% MDR with monthly repayments).

The challenging aspect though is being careful with choosing who you lend to and how much? Slice has so far been able to maintain 3.26% NPA (or the loans which were never paid back), which is right between industry standard 2-4% for credit cards.

BNPL is not a new industry. Credit Cards have been in the country for well over a century, but even now only 3% of the country has access to it. This is because of the risks that come with giving interest-free loans even for 30 days and therefore the large guardrails around issuing them.

No new startup can compete like for like with credit cards because they can be issued only to the people with a good enough credit score or a respectable and stable salary. Which effectively narrows it down roughly to only the 60 million people who already have them.

Offline BNPL services were started by Bajaj Finserv offering EMI cards at many shopping centres where a customer could buy their product and then pay their EMIs. They only had 9.8 million Indians till 2017, when they were the leader in consumer financing with over 50% market share offline, and it had been in the consumer durables financing business since 1999.

Even Simpl, founded in 2016, that launched online BNPL in India, did not get as much traction as Slice has. It has only 7 million customers since 2016 and can support a $1 billion line of credit.

The problem is that Bajaj Finserv, Simpl and LazyPay, all had to go and partner with merchants to offer their solutions, one by one.

What Slice did differently is tap onto existing customer and merchant behaviour, both at the same time. Customers could use this like any other debit card that almost every Indian has. And all Visa cards had the widest adoption possible. They back loaded these cards with a credit line and it was magic. The magic lay in the card bit, and the realisation coming only in its pivot in 2019, since starting operations in 2015 as a student-focused micro-lending platform. Positioning itself as a credit card with little eligibility criteria did the rest.

Slice was issuing over 3 lakh cards a month by June this year, that puts it in the leagues of top banks that issue as much. It said it has 12 million customers and another 10 million on its waitlist, as well as a total of $291 million in funding with $220 million in its unicorn round only and another $50 million at $1.5B a few months back.

Competitors, like Uni Cards (Founded 2020, $94 million funding), and KreditBee Cards (2021, $139 million funding) have also been quick to get adoption as lending apps do, but this was the billion dollar idea that Slice pioneered.

We wouldn’t have been writing this article if it hadn’t been for the RBI, and like every other Bollywood movie, RBI struck its regulatory hammer in two parts and an uncalled-for interval.

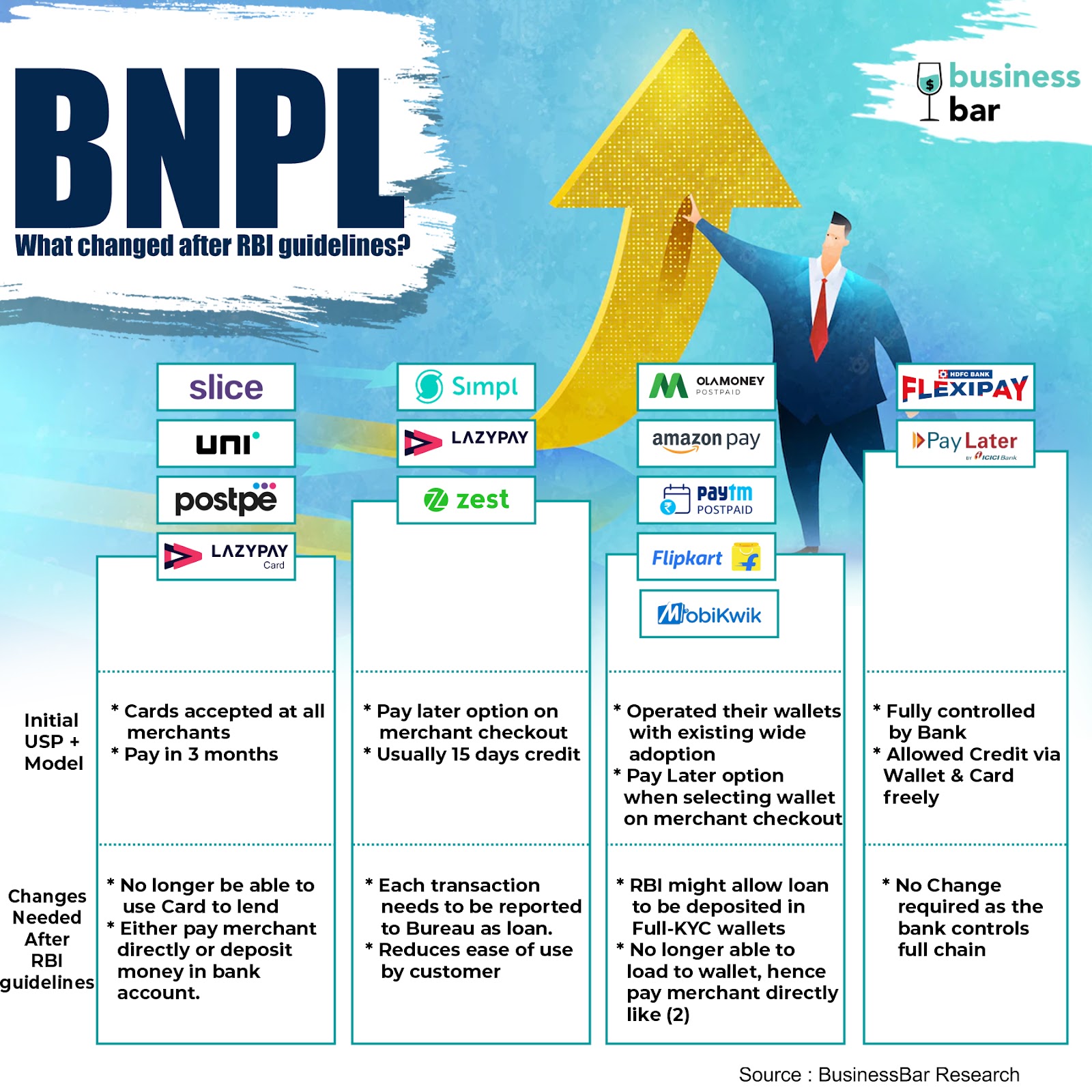

First, on 20th June 2022, the RBI issued a directive that prevented loading of non-bank Pre-Paid Instruments (PPIs) from credit lines. PPIs include the cards issued by Slice, Uni Cards, PostPe, LazyPay and the likes as well as other co-branded cards, payment cards (like Sodexo) and even Digital Wallets (like PayTM, and MobiKwik).

Obviously this notification was aimed at the digital lending space to curb the practice where a BNPL company would issue PPI cards in partnership with a bank and fund them through their NBFC (non-bank) partnerships. Almost all of them used SBM bank due to its willingness to work with FinTechs. When SBM bank had to stop issuing cards, it meant none of them could. More on this later.

The more interesting part however was that the RBI notification affected only non-bank PPIs. This meant it was possible for banks to issue PPIs and load them through credit lines offered by themselves. Hence, this left the likes of HDFC FlexiPay (that gave credit through bank debit cards) and ICICI PayLater (that gave credit via UPI) with a free hand.

By doing this, RBI effectively said that they want the entire lending chain to be either regulated (controlled by banks) or non-regulated, but not a mix of both.

Although the RBI did this with the intention of consumer safety, it left the industry in confusion. With the intention to protect customers from loans/credit that they can’t afford to repay, having already faced the wrath of the Chinese lending apps, the RBI promised to release the digital lending guidelines soon. A 50 day interval followed.

During that time, all of these BNPL companies stopped issuing new cards, and all of them stopped the pay-in-3-parts option requiring customers to clear their dues each month. But it was still credit, even if the customer pays a day later. Nobody was sure what to do though.

Credit where it’s due, RBI soonish announced the Digital Lending Guidelines on 10th August.

The RBI has made clear 3 important things

All lending and repayments must be between the bank account of the lender and the bank account of the customer. This will deal a massive blow to the likes of Slice, Uni Cards and PostPe that power their loans through prepaid cards. Even the wallet operators like PayTM will not be able to give loans through their wallets. Although there is belief that fully KYC-ed wallets might also be allowed to receive the money in the future as there is a proper customer verification involved.

There is however an exception made for co-lending partnerships. NBFCs and banks sometimes jointly extend loans, and this could be an advantage for FinTechs that have an NBFC of their own. Slice already has its own NBFC – Quadrillion Finance Pvt. Ltd, while BharatPe (owns PostPe) already has RBI approval to start a Small Finance Bank. It won’t be long till Uni Cards also gets his house in order as Nitin Gupta, CEO had said “Every fintech player should get NBFC license from RBI” as long as 9 months back.

The much bigger headache is figuring out the customer bank account. It would be an ordeal to open customer bank accounts, as that throws the fast credit approval process out of the window.

The RBI reiterated its focus on protection, and that all charges for any kind of loan given should be made abundantly clear at the beginning to the borrower. No more opaque pricing and high interest rates that put customers in trouble. Further, all the fees that FinTechs earn from the lenders for bringing customers, should not be collected from customers. This will hugely impact revenue structures for FinTechs as they would have to collect revenue from the NBFC or bank only, be it owned by themselves or in partnership.

All loans will have to be reported to the Credit Bureaus. This is a tricky spot. The BNPL FinTechs will need to record each transaction as a separate loan, report it to the bureau, then mark the loan repaid at the end of each month (or billing cycle). What this does is build the credit score for their customers and eventually they would look for more premium credit cards that offer other benefits rather than just a pay later option. Card based lenders (Slice et al) would be worst affected as they are replaceable by credit cards. The others (Simpl, LazyPay, and other wallet based) might still be okay as they are more convenient and easier to use ( read: OTP-less) than credit cards.

Whatever it may be, the “good” customers of BNPL will become credit card holders gradually, while the FinTechs would have to keep searching for the next “new to credit” bunch.

In essence, it’s a funny as well as limiting set of regulations, and it fits to see what Ashneer Grover has to say about it –

“Essentially, RBI is telling Fintechs ‘Bhai, mat karo digital lending shending! Banks se hoti nahi, humein samajh aati nahi, aur pen paper ki sale bhi kam hogi” – Ashneer Grover, BharatPe Founder in a tweet

The guidelines do put a lot of pressure on FinTechs and bring up the question, Is it really worth building, innovating and burning huge money on digital acquisitions? When in the end you have to either (a) end up as only a service provider to a bank to give traditional loans or (b) put your own capital as an NBFC to lend cash into, again, bank accounts only.

In short, the RBI has tied their hands to work how banks work, but with lesser access to capital.

A bank can open a shadow bank account, and put money into them to be spent from a PPI card or any mode, and that too with access to cheap capital (5.4% repo rate from the RBI and CASA – current accounts and savings accounts)

But a FinTech can only be, more or less, a digital acquisition channel.

The BNPL companies that do have an NBFC of their own certainly have an advantage over their peers but they are far inferior to banks. And the NBFC capital comes at the cost of their equity being funded by VCs, which is definitely not cheap and is limited.

Those that don’t have their NBFCs, don’t have an option but to pay their NBFC partner anywhere between 9-15% p.a for access to that capital. Recently Quadrillion Finance raised funds at a 11.5% interest rate on corporate bond platform WintWealth.

And even with a higher MDR of ~2%, their revenue can be estimated at 24% interest p.a. on whatever they lend. But with the 2% rewards that is a big attraction for the cards, it leaves little to no room for any of them to even hope of turning a profit. Further with lending going into bank accounts, the MDR revenues will go for a toss, and new revenue generating methods will have to be found.

It is entirely possible that RBI might come up with more guidelines in the future that will affect them again. Regulators and FinTechs are always running a cat and mouse game, where the winners are, most likely, none other than banks.

The RBI has given the industry until November 30th to comply with their new guidelines, and to say that it will be exciting is an understatement. Although some like Simpl and LazyPay can operate with little changes, the big ones, SUP (Slice, UniPay and PostPe) will need to overhaul their products. The same products that VCs paid top dollar for.

Basically the entire digital lending space has been about providing access to credit to people who have been kept out of it because they don’t have a credit score because they haven’t taken credit yet. It’s a tough circle to break into and people do only via loans/CC that they get based on their salary.

And the current success of the BNPL space has unequivocally demonstrated that there is definitely consumer demand for credit at the point of sale. There is merchant demand too in favour of more orders. But the new RBI guidelines deemed the current methods, used to fulfil such demand, unlawful.

Nobody can paint a clear picture of what the new methods are going to be, until the 30th of November 2022, when we see them deployed. But if there is demand on both sides, market forces will act. If not, we might see the merchants developing their own Pay Later services akin to the big ones like Flipkart and Amazon. And then FinTechs will move to developing APIs and white-labelled solutions that enable small or medium merchants to do so easily.

Another interesting sector that is also commerce-enabling and could potentially be a parallel to BNPL is SNBL – Save Now, Buy Later. It is still an emerging sector and fairly nascent. What it does is flip the Pay Later part of BNPL. Consumers can start saving up for what they want to buy on a SNBL app, and buy the product when they have saved up their desired amount. It enables commerce by making it easier for those unable to get EMIs. Prominent Indian players in this space being Tortoise, Hubble, and Multipl – all with seed funding a total of $9 million. This space deserves a full piece on its own, but in case you are curious please feel free to reach out.

SNBL and BNPL both have rather fascinating times to come. One to chart its early growth trajectory and another to innovate around the growing roadblocks in its way.