Categories

Dearest Readers,

Truth be told, the writing of this article has been precariously procrastinated since our cinephile author is rather easily distracted by the newest shows on Netflix almost every time she sits down to pen this. No wonder OTT has taken the entertainment space by storm. And together with the pandemic, OTT might have played a prominent role in the recent developments within the Indian entertainment space – the topic of today’s article. And while our author is no Lady Whistledown, let’s just hope that this article is as good a read as her gossip sheets!

(Well, clearly, someone has been binging on the latest season of Bridgerton! Huh!)

And now that we have THAT out of the way let’s dive straight into our article for today –

Consolidation and Cooperation seem to have become a norm in India for the leading players across multiple industries. Some prominent mergers from recent times come to mind – Financial sector: HDFC – HDFC Bank Merger (2022), Media & Entertainment: Zee – Sony Merger (2021, completion expected by Aug 2022), FMCG: HUL-GSK Merger (2020) and Telecom: Vodafone-Idea Merger (2017). One of the recent additions to this list is, ofcourse, the PVR – INOX merger that caught everyone by surprise.

It was just about a month ago when PVR and Cinepolis, India’s largest and fourth-largest multiplex chains, respectively, were reported to be in advanced stages of talks of a potential merger. And so, the announcement of the PVR-INOX merger in late march was quite the curveball. (FYI – INOX is the second-largest multiplex chain in India, behind PVR)

And while it might be too early to comprehensively study the merger itself and how it will see itself to fruition, one can definitely try to break down what went on behind the scenes in this Silver Screen industry that led to the cooperation of these two giant players.

The Indian Silver Screen at a glance

One might be amazed if we talk about the sheer scale of the film industry in India, which produces almost three times as many movies as Hollywood. About 2400 movies were certified for release in India in 2019. In terms of financials, however, India lags far behind Hollywood – earning gross revenues of ~USD 2.58 Bn (INR 191 Bn) against Hollywood’s USD 11.32 Bn in 2019. {Using pre-pandemic numbers)

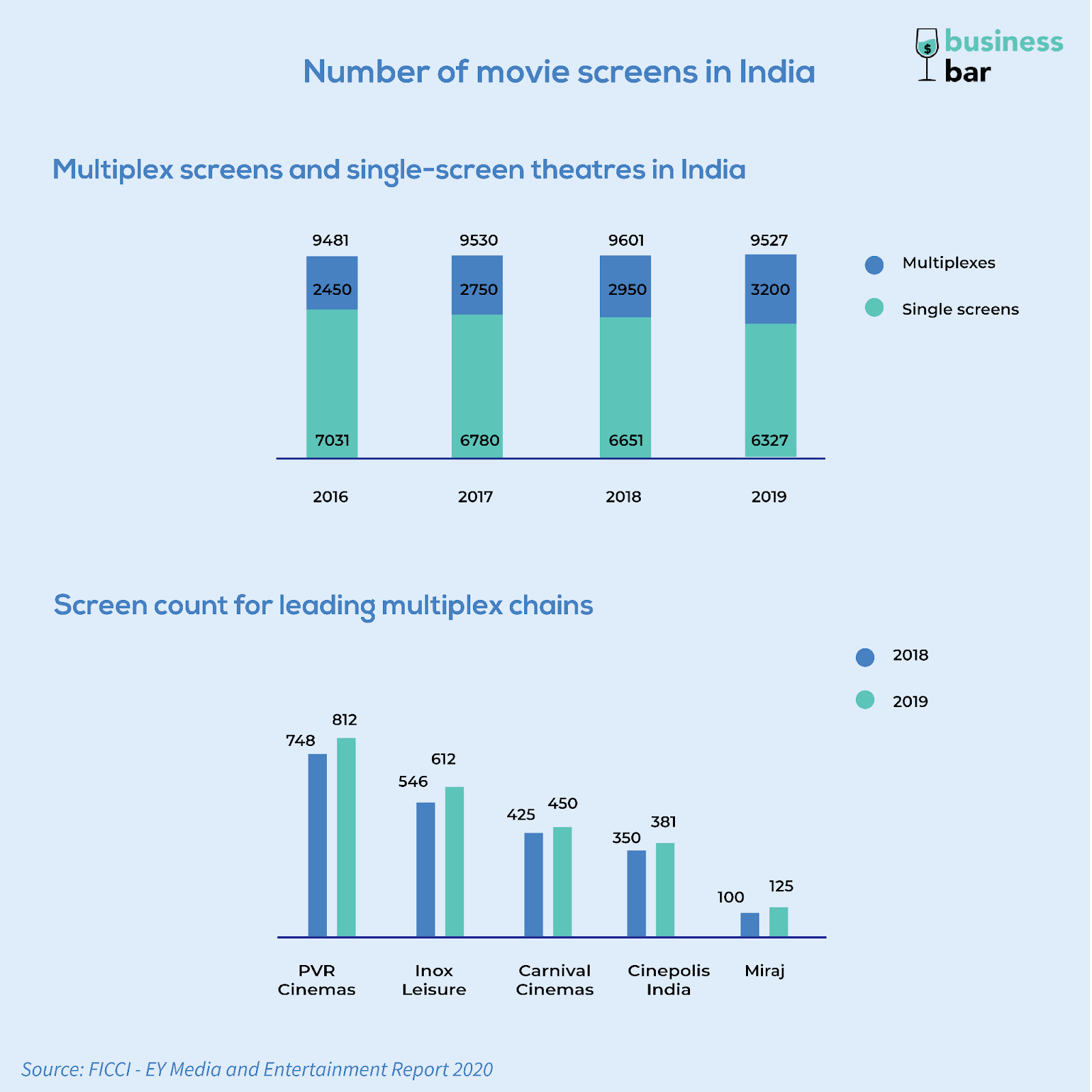

This is very well reflected in the atrociously low screen density – ~8 screens per million population in India (down from >10 screens per million population in 2010), in contrast with the same metric being 37 in China and 124 in the US. One should note that the screen density in India varies drastically across India, with as many as 20 screens per million population in South India to a meagre ~1.5 screens per million population in North-Eastern states. Clearly, there is potential for expansion and multiplexes are vying for it. But if there’s a victim in this narrative, it’s clearly the single screen theatres.

In 2019, India had 9527 screens, only 3200 of which were accounted for by the multiplex chains. The rest were single-screen theatres, the numbers of which have dwindled from ~9700 in 2010 to a meagre 6327 in 2019. The pandemic further aggravated the situation for these single-screen theatres as they struggled for survival.

The reasons for the shut down of single screens are manifold. Increasingly, audiences prefer multiplexes for reasons pertaining to great location, better technology, superior amenities and F&B services. Moreover, for customers, it’s often not just about watching a movie, but a full day experience complete with shopping, movie and dinner. Hence, they prefer a one-stop location for all their planned activities – a mall. The choices of movies showing in a theatre also become a key deciding factor – a big disadvantage for single-screen theatres. For this very reason, single-screen tickets are usually priced significantly lower to even compete with the multiplex chains in prime locations. The financial disparity is so much that even though single-screen theatres account for ~65% of total screens, more than 50% of the box office revenue is earned by the multiplex chains.

Moreover, the entire cinema industry in India is over-regulated with each state having its own set of rules and regulations and each city, having its own licensing authority. The yearly renewal of licenses is subject to the approval of 50-90 permissions depending upon the location of the theatre – leading to an extremely complicated procedure. While the multiplex chains with deep pockets are able to navigate this, it becomes extremely difficult for small theatres with only one screen. And given their small scale, they don’t have any bargaining power with film producers and distributors, leading to meagre margins and a perpetual cycle of misfortune. With the pandemic in the picture, the revenues have been virtually zero and combined with the high maintenance costs – an increasing number of single-screen theatres are shutting shop.

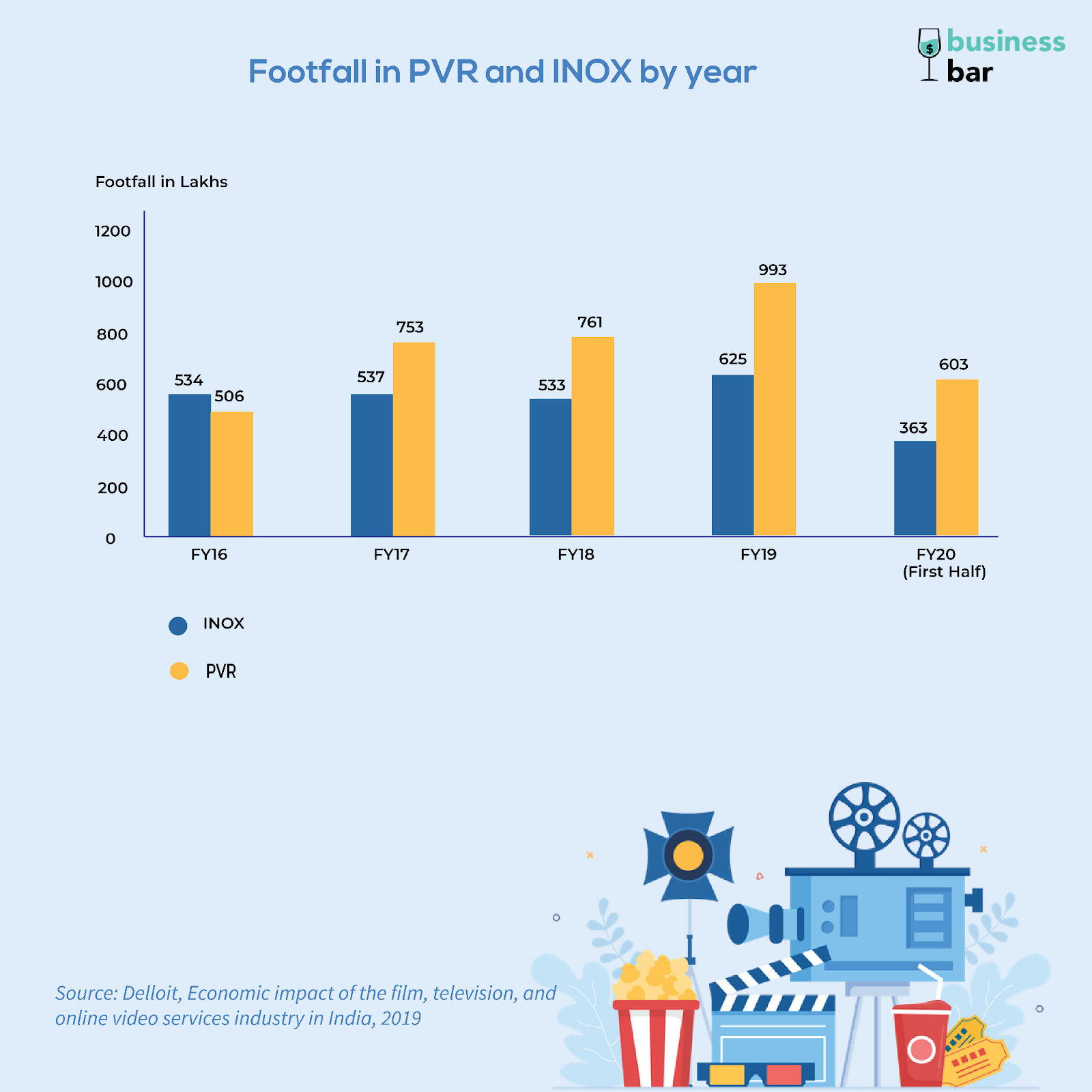

All this while, multiplexes have been expanding owing to an underpenetrated market. However, their growth has been considerably slowed down due to COVID-19. In FY20, PVR and INOX added 87 and 85 screens respectively. In contrast, only 30-35 screens were added by each in FY22.

Even before the pandemic, single-screen theatres across India were shutting down faster than the multiplexes were expanding, leading to a decline in the total number of movie screens in an already under-penetrated industry.

Understanding the fundamentals of money-making movie theatres

We’re sure you can recall atleast one instance where popcorn at a movie theatre cost you equal to or even more than the ticket price. Clearly, tickets are just one revenue stream of many for theatres. Let’s break it down!

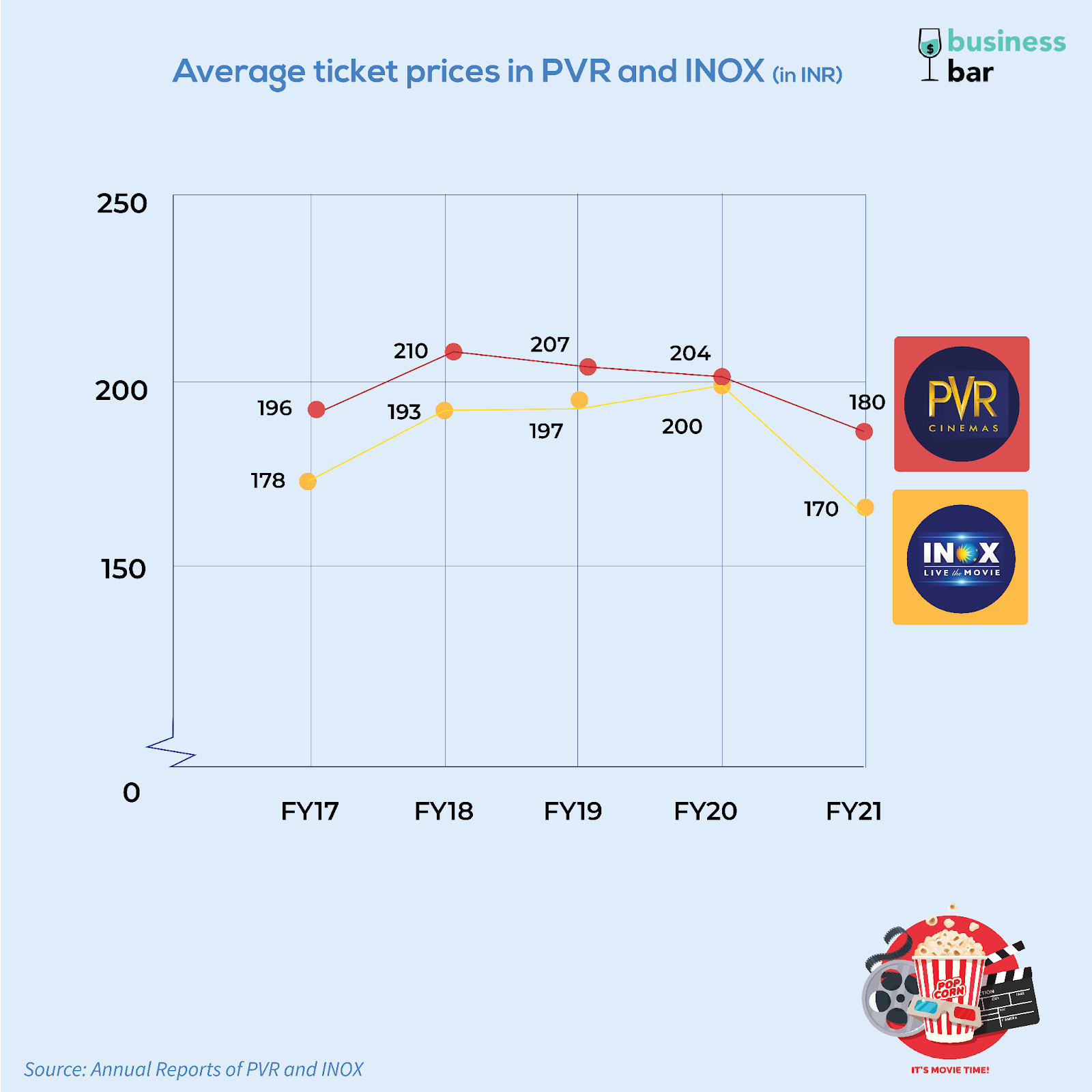

Box Office Collection: Every time you purchase a ticket on the theatre ticket counter, a fraction of it goes to the movie theatre and the rest goes to the filmmakers based on the negotiated revenue share of the producers. This share varies widely for different theatres and also changes basis the time a movie has spent at the box office. Ofcourse, leading multiplex chains have an upper hand over smaller players and single-screen theatres in this regard. For multiplexes like PVR and INOX, pre-Covid, the revenue share of producers stood at around 50-52 percent in the first week, with the rest going to exhibitors. This is ofcourse the biggest revenue stream for any theatre.

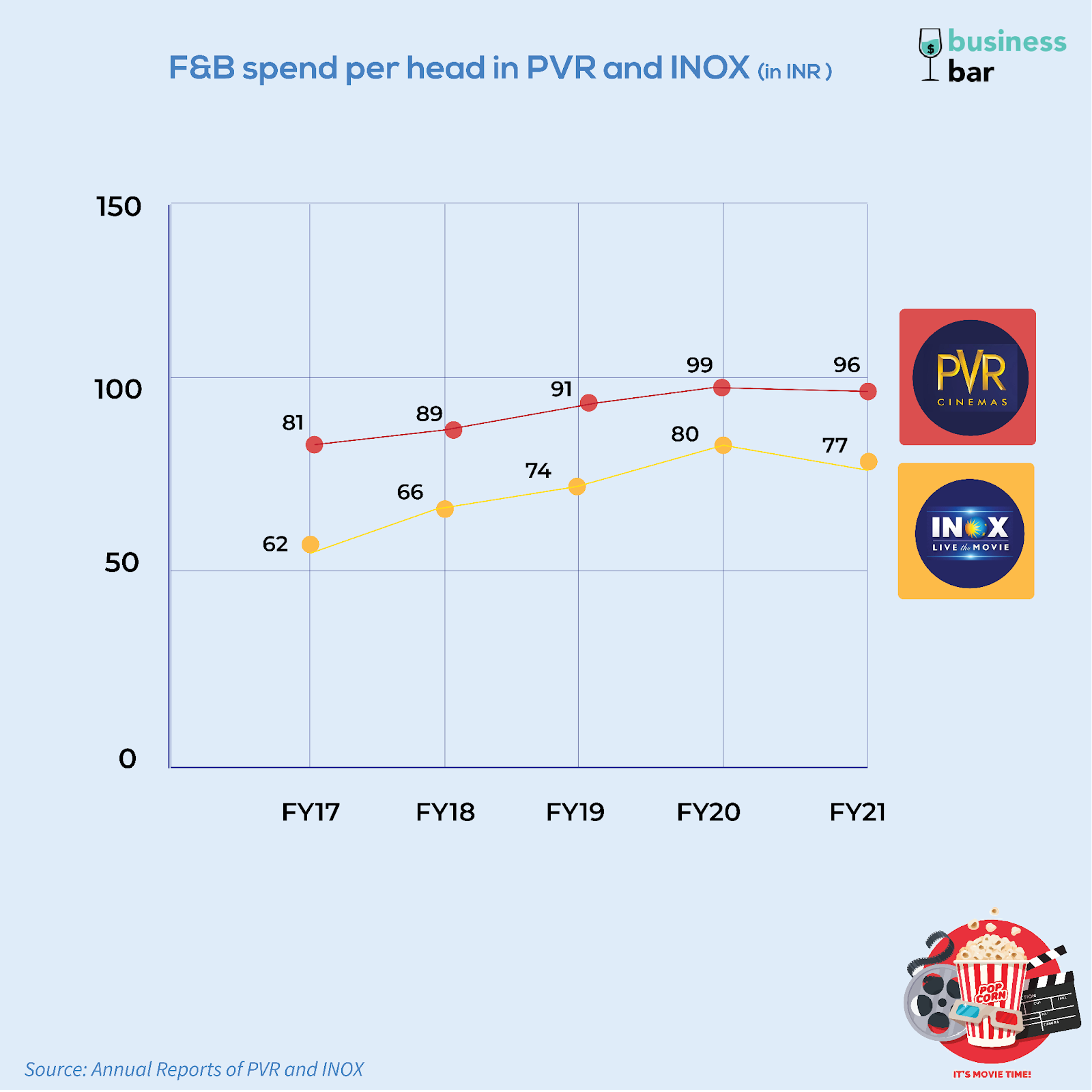

Food & Beverages: Theatres earn a handsome about 25% of their revenue from the sales of food and beverages. And they have started to accentuate it more and more. Increasingly, the F&B spaces in movie complexes aren’t just popcorn and soft drinks, but many other snacks. Multiplexes like INOX Leisure and Cinepolis even started to offer their F&B services to non-cinegoers and collaborated with celebrity chefs to develop signature dishes. PVR even created an in-house brand called Simply Sushi

Advertisement Services: Another big source of revenue for film exhibitions is the revenue earned by displaying advertisements in the cinema hall before the movie starts and during the intermission. The advertisement revenue is considerable and dropped drastically due to the pandemic.

Convenience Fees: When you purchase your ticket on a digital platform (theatre website or other third-party platforms), you pay an additional charge over and above the ticket price. Together it accrues to a considerable revenue stream for the multiplexes. The number of tickets purchased electronically vis-a-vis those purchased at the ticket counter has increased gradually over the years. PVR charged an additional INR 5 – INR 25 per online ticket, depending upon the platform of purchase.

The OTT Threat ?

Movie theatres and OTT platforms co-existed in peace before the pandemic. Yes, OTT has grown massively in recent years – a massive increase from 32 Mn subscribers in 2019 end to about 70-80 Mn paid subscribers by the end of 2021. Indeed, the pandemic led to some blockbuster years for OTT. But rather than being a substitute to theatres, it infact complimented them. Despite the OTT boom- 2019-2020 was also the strongest year for Indian theatres- both revenue and footfall-wise. Big budget films would usually release in theatres and would take a few months before they premiered on OTT or television. OTT was seen as a platform primarily for non-mainstream and foreign-language content, along with mainstream movies that had already been released at the box office.

Infact, there were theatre-OTT partnerships like that of PVR and MUBI in the form of the MUBI GO app. The collaboration resulted in a mechanism where every MUBI subscriber gets a free ticket every week to watch a MUBI handpicked movie in a PVR theatre.

The picture ofcourse is not all rosy and theatres and OTT do compete on some levels.

Post box office release, movies have an exclusive-theatre window where they can only be viewed in theatres and not on other digital platforms or television. Until a few years ago, this window was typically 6 months but has now reduced to 45-90 days. For Bollywood movies specifically, there’s typically an 8-week gap between the theatrical release and digital premier.

In 2017, theatres and OTT accounted for 62% and 5% of a film’s revenue respectively. In 2019, the share of theatres had decreased marginally to 60% and OTT’s contribution had risen to 10%. While OTT has been on a rise, the competition is not even close.

As theatres were closed due to the pandemic, the release of prominent movies was either postponed or taken directly on OTT platforms. The Ayushman Khurana- Amitabh Bachhan starred Gulabo Sitabo became the first mainstream Bollywood movie to change its plans from a theatre release to an OTT release. Many mid-budget and some large-budget films followed path – Shakuntala Devi, Dil Bechara, Ludo, and Sadak 2, Coolie No. 1 – were all released on various OTT platforms. Quite a few high-budget movies however were postponed due to COVID – This includes the now released Gangubai, Sooryavanshi and RRR, and some still awaiting releases like Shahid Kapoor starrer Jersey, Akshay Kumar’s Prithviraj etc.

While the recent success of Gangubai and The Batman at the Box Office is a strong indicator that people are eager to return to the larger-than-life experience of watching a movie in a theatre, it remains to be seen if it’s just the post-blues excitement or a consumer preference in the long term. Will the convenience & accessibility of a 6×3 inch mobile screen or an 8×12 inch laptop screen wipe out the cinematic experience of a 25×50 ft theatre screen? – In all likelihood, the answer is No.

They will most likely continue to co-exist, though with some critical shifts in the workings. Certain nuances are important to be understood in this context. The pandemic has made the filmmakers more open to releasing movies online and one can expect this to be the case, especially for mid-budget movies. A recent study found that viewers are more likely to watch a content-driven movie in theatres and ratings & reviews play a crucial factor in the decision making. In some cases infact, OTT drives people to theatres as it creates an appetite for content consumption – Fans of older sequels of franchise movies to watch the release of a new one. Marvel, DC, and Bond movies come to mind. One key realisation is that the balance in Theatre-OTT coexistence post-pandemic is a little bit tipped in the favor of OTT as compared to the pre-pandemic scenario. And while the theatres are looking for a strong recovery in the upcoming years, they will have to fight with OTT a bit harder than they had to before. Which is probably one of the reasons, they’re joining hands to come back stronger than ever.

The PVR and INOX Leisure Merger

Consolidation has been on the cards for Indian movie exhibitors who observed a sharp decline in their revenues & profits due to the pandemic but are now optimistic about the future outlook and looking to make a strong comeback.

Just over a month ago, PVR was reportedly in merger talks with Cinepolis and INOX, apparently, was seeking to acquire Carnival and Miraj cinemas. But when the two leading competitors – PVR and INOX decided to merge instead – the implications of it are far greater!

In the official merger announcement on March 27, Ajay Bijli, Chairman and Managing Director of PVR said “ The film exhibition sector has been one of the worst impacted sectors on account of the pandemic and creating scale to achieve efficiencies is critical for the long-term survival of the business and fight the onslaught of digital OTT platforms”

Let’s for a second assume, that the deal goes through! (A question we will come back to soon)

With synergy in operations and over 50% market share within the multiplexes, PVR and INOX expect benefits of the merger on both revenue and cost sides. Predominantly on the revenue front, the merged entity will benefit from the higher advertising revenue (due to increased footfalls) and higher convenience fees revenue (due to better negotiating power with aggregators like Paytm and Book My Show). They will also have much higher bargaining power in terms of content costs from production houses, rentals, F&B sourcing, and savings in many cost items. Estimates suggest that the synergies could lead to as much as ~25% increase in PAT by FY24.

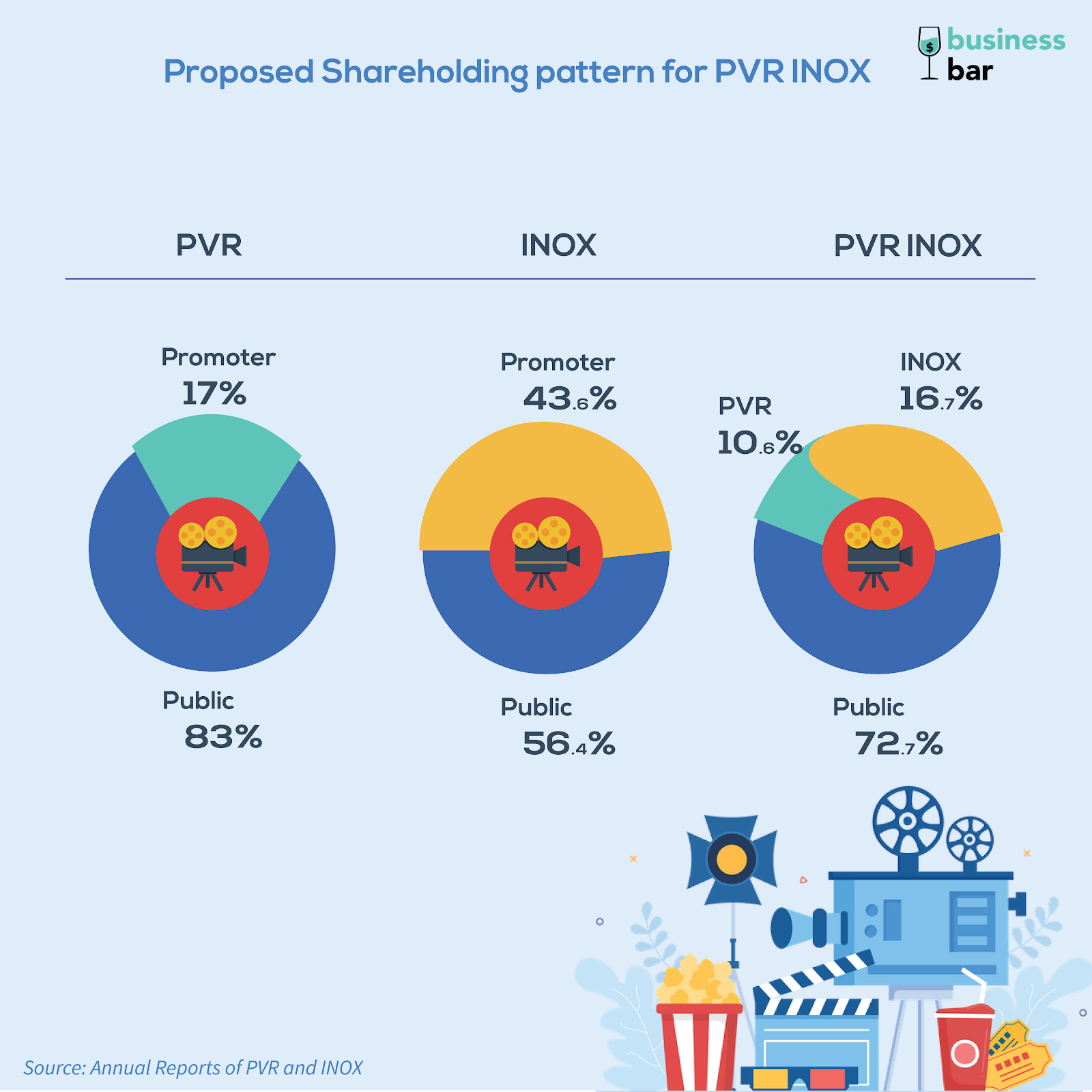

The merged entity will be called PVR INOX Limited and the existing screens will continue to be branded under PVR and INOX respectively but the new ones will be branded as PVR INOX. PVR currently operates 871 screens across 181 properties in 73 cities and INOX operates 675 screens across 160 properties in 72 cities, PVR INOX, hence will become the largest Indian film exhibitor, operating 1,546 screens across 341 properties in 109 cities. (about 45-50% market share within the multiplexes)

PVR INOX has already spoken about adding ~2000 new screens in the next seven years and increasing penetration in Tier-II, III and IV cities. We can expect the number of screens to grow quite quickly as both companies already had new planned screens in the pipeline- PVR planning 120-130 screens and INOX ~100 screens. 10-15% of screens are planned to be in the premium category. The merged entity would invest a Capex of Rs 2.5 crore per screen as part of the expansion plan.

PVR CMD Ajay Bijli and INOX Leisure Director Siddharth Jain have also indicated that film production might be on the cards for PVR INOX merged entity. The pandemic has taught that it’s better to not put all your eggs in one basket and revenue diversification is key to hedging the risks in uncertain circumstances.

From a shareholding point of view, INOX promoters will become co-promoters in the new entity with the existing PVR promoters. PVR promoters will hold a 10.62% stake, while INOX promoters will hold a 16.66% stake. The two players have decided on a share swap ratio of 3 shares of PVR for every 10 shares of INOX. The swap ratio is said to be in favour of INOX investors by 12%, probably owing to its probably due to its zero net debt situation compared with PVR’s net debt at INR 857 Cr. The merger is an all-stock amalgamation, one that is great for both PVR and INOX since the massive cash burnt and losses made by them in the recent years.

In terms of overall valuations, analysts valued Inox at INR 6500 Cr and PVR at about Rs 11,000 crore. The combined entity valuation could be higher by 25-30%, creating nothing short of an entertainment exhibitor behemoth. The current valuation of the merged entity is INR 17,400 crore and has the potential of reaching over INR 22,000 crore by FY24, with estimated revenues reaching INR 6800 Cr in FY24.

Although it came as a surprise, the ‘blockbuster merger’ was well received by the Indian financial markets- On Mon 28, March, the day after the announcement, PVR and INOX stock prices hit their 52-week high. PVR and INOX stock prices surged by ~10% and ~20% respectively on both BSE and NSE.

Will the deal come through? What about the competitors?

If this is a movie, and our two protagonist multiplexes are lovers waiting to be reunited – there has to be a roadblock and a villain in the climax! (We’re here for the movie puns!)

Let’s go back and question our assumption in the previous section that “The deal comes through”. But why would it not?

Timing is crucial when it comes to the PVR INOX merger, as the deal aims to fruition with no immediate review by the Indian competition authority. In 2014, Carnival’s acquisition of 238 screens of Reliance Media Works had to undergo CCI clearance. In 2015, PVR had also required CCI (Competition Commission of India) clearance to acquire a much smaller DLF Group owned DT cinemas’ 39 screens.

How then will the PVR INOX deal conclude when they together account for more than 50% share of total multiplex screens in India?

The caveat is that the Indian merger control regulations exempt deals where the entities merging or the target entity has assets below Rs 350 crore or revenue below Rs 1,000 crore in the preceding financial year. This exemption was previously valid till March 29, 2022, and PVR & INOX announced their merger on March 27. (The exemption has been further extended for the next 5 years)

So in all essence, PVR and INOX have cleverly leveraged their devastating performance in the recent financial years due to pandemic- to quality under the exemption! A route for them to possibly bypass CCI altogether.

However, CCI could still come knocking, especially since the 2 biggest players are joining hands and this might put the competition & other stakeholders at a significant disadvantage.

If PVR and INOX merge, PVR INOX will have a 44% – 50% market share within the multiplexes. If we add single-screen theatres, this goes to less than 20% and if we further add OTT to the mix, this is further diluted.

Film producers & distributors, F&B suppliers, and Ticketing platforms would have lesser bargaining power and competitor multiplex chains would be at disadvantage struggling to compete. In far fetched scenarios – This could virtually lead to a monopoly. Concerns have also been brought up that PVR INOX might raise ticket prices. However, PVR and INOX have been trying to reassure the stakeholder that they will not act funny.

If all goes well, PVR CFO Nitin Sood said that the merger would be completed within the next 6-9 months.

Only time will tell whether or not CCI will intervene on account of attempted anti-competitive behaviour or not. If it does, it could direct behavioural and structural remedies such as ticket-price caps or divestiture of screens, impose a fine or even split the enterprise—something unprecedented in the history of CCI.

One can only wish our protagonists all the very best!