Categories

“An IPO is not the end but actually the beginning.” – Nithin Kamath, Zerodha

While Nithin meant the above to alert the founders, recently there’s something that has begun to alert the IPO market in general and might threaten to change the way private companies go public. But before we start talking about SPAC, let’s brush up on how an IPO works.

An IPO or an Initial Public Offering is when a private company offers shares to the general public. The company is able to raise capital from the public while the public gets to be the shareholders or more crudely, partial owners of the company.

What if we told you this is not the only way to go public. Sometimes, a private company can take a different route to achieve the same outcome of going public and raising money. Allow us to introduce you to an offbeat way of going public via Special Purpose Acquisition Companies or SPACs.

The public and institutions invest in a public offering of a company (let’s call this company a SPAC), only this time, the company has no operations and no real business. All the company has is

1) funds raised from the public offering which are kept in a secured bank account

2) a team that has a fixed tenure of time to identify the right private company to merge with this SPAC

Once the team is able to identify and close a merger deal of the SPAC with the target company within the stipulated time, usually 24 months, the original shareholders of the SPAC receive shares of the now-public company. This post-merger entity has an actual business as opposed to the SPAC which was just a shell. See, the same outcome as promised, an earlier private company raised capital from the public by issuing them stocks, without filing for an IPO.

In the rare case of the management team (more rightly called sponsor in this context) being not able to reach a deal within the time limit, the SPAC is dissolved and the original investment plus the accrued interest is returned to the original investors. From 2003- August 2020, only 90 out of the 477 SPACs that got listed were liquidated, amounting to ~ $12Bn out of $100Bn+ raised as per spacdata.com.

SPACs have been raising record money and have arguably become the hottest investment vehicle even in this year full of uncertainty.

So now you know what a SPAC is and that they’re the buzz of the town. But as Einstein said, “Any fool can know. The point is to understand.” And the best way to understand what SPACs unfold for the financial system and corporations is to look at how a SPAC looks like from the perspectives of stakeholders involved.

The fundamental difference between a traditional IPO and a SPAC is that at the time of public offering there’s no actual business that the investor is aware of while committing his money to a SPAC. And that’s why SPACs are often called ‘blank check companies’. It’s just a blank check seeking the right company to fill in the name section on the check. This information scarcity might sound as a trigger warning for those who believe in the investment philosophy of invest only in what you understand. But it is important to understand that even the absence of any light on the company you’re betting on is irrelevant as an investor in a SPAC. It is because it is not the business that you’re betting on, but the ability of the management team of the sponsor to identify the right target company and close a quality merger deal with it within the time frame.

It is the responsibility and duty of the sponsor to have a merger done and thus the negotiations of the stake sale of the private company to the SPAC occur behind closed doors. Hence SPACs also enable retail investors to get exposure to private equity kind of deals even with ticket sizes as low as $10, often in new and lesser understood business.

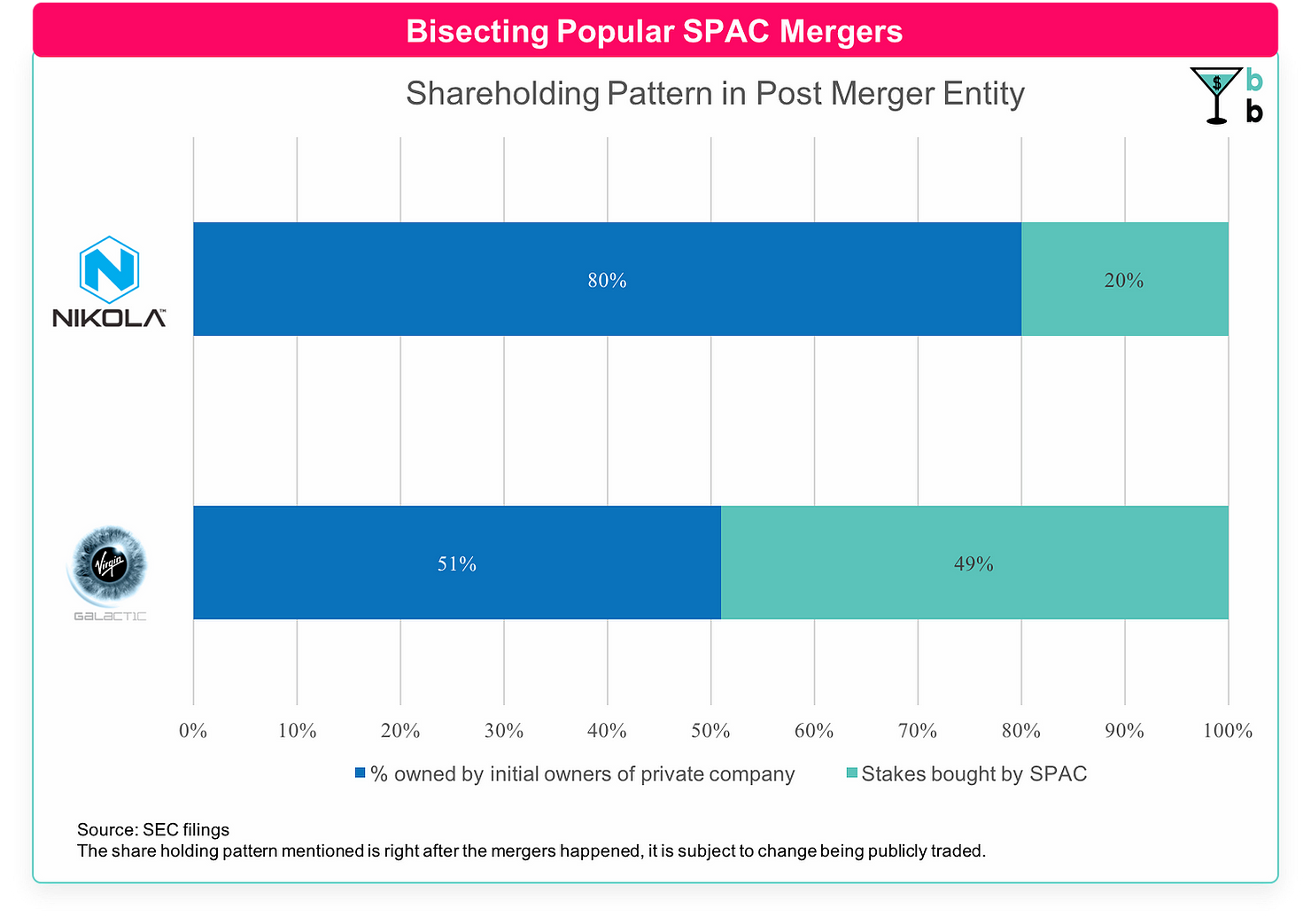

This also brings the opportunity for a retail investor to outsource expertise required to value unconventional businesses, where there might definitely be a business opportunity but not a proven business model yet. Remember Virgin Galactic, the ‘space tourism’ company by British billionaire Sir Richard Branson, in October 2019 it became the first space tourism company to go public and yes, it was after it merged with a SPAC sponsored by Chamath Palihapitiya’s Social Capital.

The Sponsors of a SPAC are usually known hedge fund managers or investment professionals. The famous hedge fund manager Bill Ackman went on to raise $4Bn in 2020, a billion dollars more than the initially planned sum. Now Mr. Ackman is on a hunt for what he calls a ‘mature unicorn’ and that curtails him to a universe of an odd 150 private companies to find one to marry his blank check company – Pershing Square Tontine Holdings.

$4B by Bill Ackman is the highest amount any SPAC has raised to date.

Remember Moneyball? The movie, Brad Pitt, baseball? Or the book, Michael Lewis?

Well for those who don’t, Billy Beane was the general manager of an under-budgeted and underdog baseball team in America. In 2002, he built a team using Sabermetrics or in a simpler language, he focused on player analytics and empirical data. The team went on to win 20 straight games that season, an all-time record. This changed the way teams were drafted in not only baseball but significantly shaped the adoption of sports analytics as we know it. But what’s the relevance of Billy Beane, an ex sports-team manager, and SPACs, you may ask.

What if you wish to be the co-owner of a sports team in a popular league without spending millions of dollars? Well, that is the dream that the investment firm RedBird Capital Partners sold when they partnered with Billy Beane and raised $575M for the blank check company Red Ball Acquisition Corp. in August 2020. After all, who better than Billy Beane to find the right pick here.

Thus, usually, sponsor groups also involve veteran industry-specific executives that not only assess the right targets but also reinforces public confidence in the SPAC’s ability to lead to a successful listing.

The greatest benefit SPACs bring to the Sponsors is the compensation structure of the SPAC. While the Sponsors usually chip in around 5-8% of the capital in the SPAC, the ownership of the sponsor in the post listing entity is to the tune of 20% of the stake that all the SPAC investors hold. This is achieved by the financially engineered design of the SPAC involving financial instruments called warrants and founder shares. There are no other incentives that a Sponsor gets other than this, unlike the fees that investment banks charge for traditional IPOs and M&A transactions.

As we’ve seen, SPACs are just another way of going public when viewed from the private company’s lens. So the more essential question is what are the benefits of opting this alternate route to a listing?

In the crudest essence, for any private company SPACs are a way to outsource the IPO process. Instead of filing for the long traditional IPO process with regulator and spending time and money prepping the company for a public listing, merging with the SPAC is cheaper and more certain on the price point because the nature of the deal is more like a private equity deal where someone has already gone through the trouble of raising money from the public and pooling it together.

So if the core business of the company is one which is not yet well understood, such as Space tourism like we saw in the case of Virgin Galactic or Hydrogen powered trucks as is the offering of Nikola which also got listed after merging with a SPAC, it looks prudent to opt the SPAC route as the risk of loss of public interest in the company due to lack of business understanding gets transferred to the more sophisticated investors comprising of the SPAC Sponsor Group.

Volatility is another enemy of IPOs. Public sentiment can very well turn upside down from the time a company decides to file for an IPO to the time of expected listings. Airbnb is the best example for the case. In 2019 Airbnb announced plans to file for an IPO in 2020, little did they know that the months to follow would be painted by history as the time of the greatest crisis that the hospitality industry has ever seen.

Thus, if market sentiments are ripe for the business of the company and it looks like the best time to go public, SPACs can help reach the listing day way quicker than the time that a traditional method of filing for an IPO with the regulator will take, thus helping in capitalizing on the opportunity which otherwise might have been lost in the months (or sometimes year) that the IPO procedures take before listing. And in early September this year, Bill Ackman tried to sell the same speedy SPAC solution to Airbnb who have revived IPO plans after looking at the recovery of both, their booking numbers and the stock market. Initial reports suggest that Bill had to take “Thanks, But no thanks” for an answer from Airbnb.

The COVID crisis and it’s impending volatility shattered lots of IPO dreams in 2020, and hence have made SPACs ever so popular.

So we saw how the additional layer of a ‘sponsor’ and alteration in the chronology of events of an IPO timeline creates what is called a SPAC, which provides new avenues to all sorts of stakeholders. The public gets the exposure of PE like deals at low ticket size. With SPACs, the institutional investors and HNI investors have to commit their capital only for 2-3 years before entering a deal as opposed to typical PE funds which are long term and capital calls come quite late. The private companies get a quicker and more certain route to go public. The sponsors benefit from dealing with higher capital and by gaining a stake in the target company at highly discounted prices as compared to if they had approached the target in isolation of the SPAC.

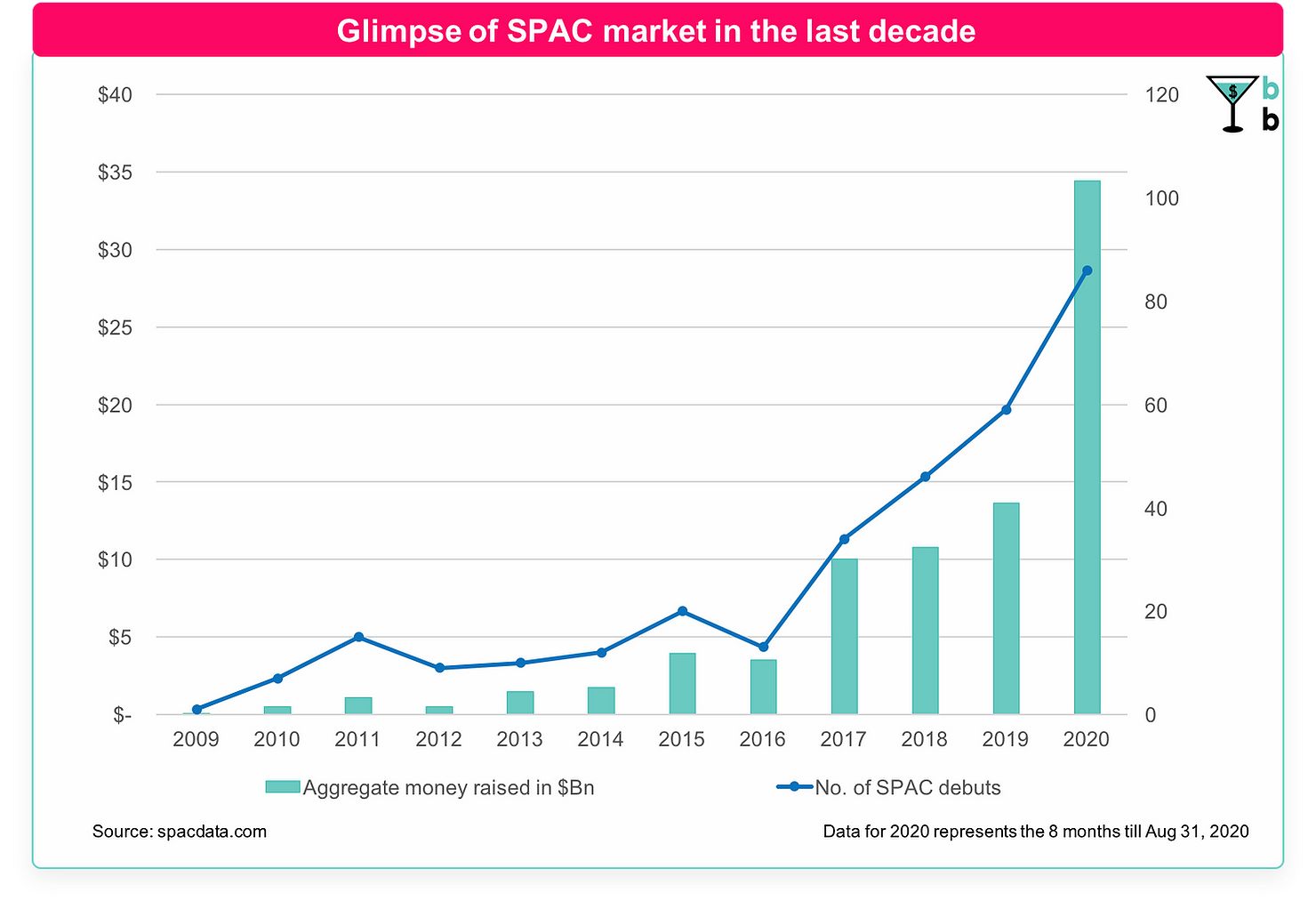

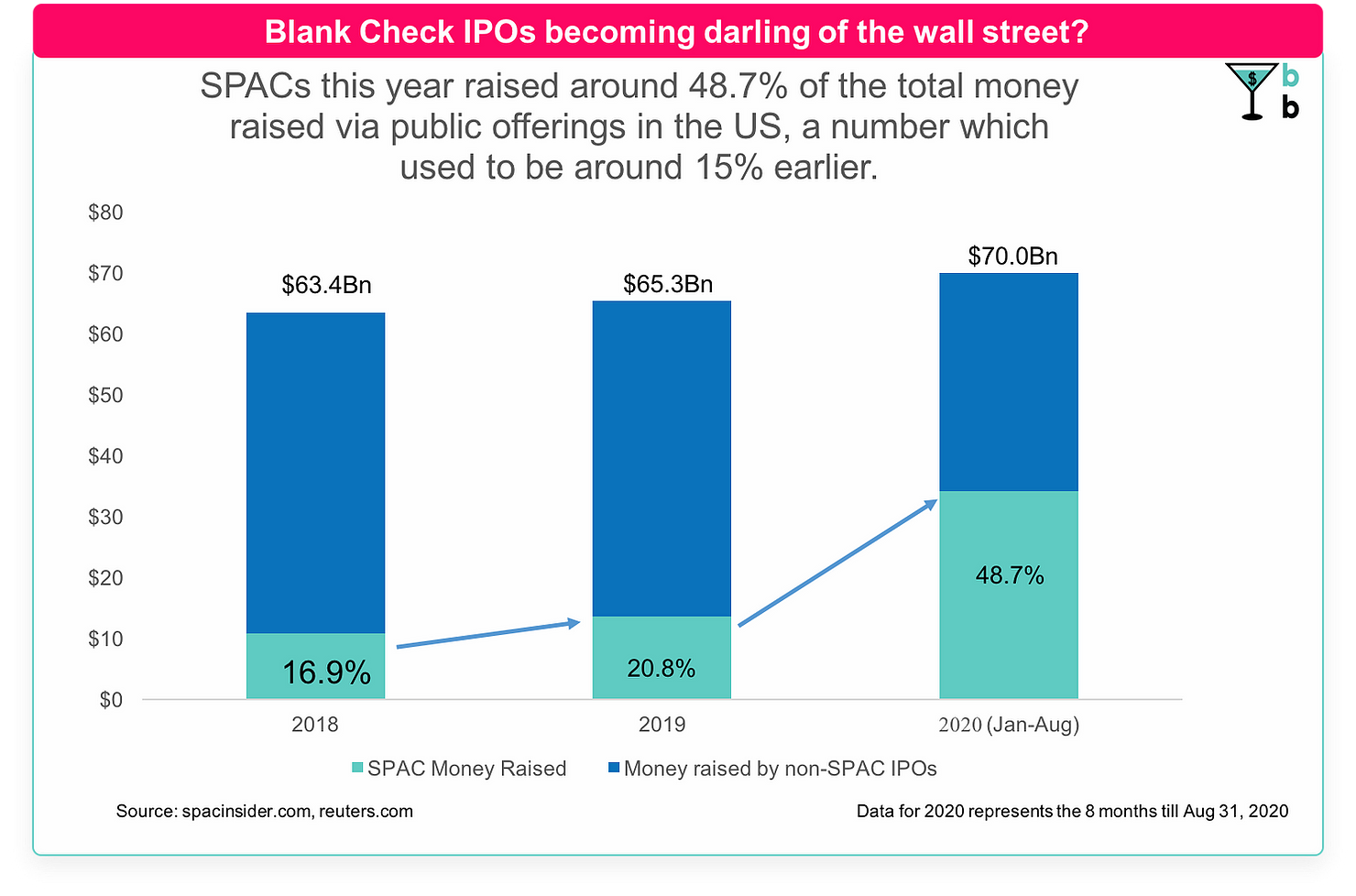

No wonder all this has made SPACs extremely popular in recent years, so much so that in the US, SPACs raised more than $34Bn in the 8 months of 2020 till august, as opposed to just $13.6Bn in the whole of 2019 which was itself a record.

But can SPACs replace the traditional IPOs? Although the increasing popularity might bring in substantial permanent changes to the IPO market, there are a few points that might pull the brakes on the SPACs in the future.

Going forward, the enemy of the popularity of SPACs could be the popularity of SPACs itself. With each successful SPAC listing, there’s more money looking to acquire private companies of appropriate sizes. As of the first week of September 2020, there are 119 SPACs sitting on a pile worth $41Bn who are looking for acquisition targets.

This creates an excess supply of capital in the M&A market but it doesn’t affect the number and size of businesses that are ready to go public. While the IPO market is a real-time indicator of the companies feeling ready to go public, SPACs try to front-run this sentiment. This coupled with the pressure of ticking timer of 24 months on the Sponsor groups can hamper the valuations from the investors’ point of view as a lot of desperate SPACs rush to convince a handful of IPO ready companies to merge with them.

Although, respecting the fact that once derided and dismissed because of their shady past, SPACs, as an M&A and finance tool, have shone during these troubled times. The historical performance of SPACs in terms of returns has been sub-par with that of traditional IPOs and it is only a handful of SPACs that have given multi-bagger returns in recent times.

As we have seen that unconventional and unestablished businesses prefer a listing via SPAC mergers, companies that already have a sound presence and robust numbers still prefer the traditional IPO route.

Also, there’s one stakeholder group that might be worried about the rise of SPACs – the regulator. Consider regulators as the police of the financial markets, like the SEC in the US and SEBI in India. As we have seen that merging with SPACs to go public is quicker for private companies because then they can circumvent the lengthy and tardy process of filing for an IPO, such as preparing the red herring prospectus and other such tasks. While there is still some amount of disclosure involved in a SPAC merger, it is definitely less than that in case of an IPO. Thus the regulator would wish to look into the fact that, is this speed that SPACs offer in taking a company public coming at the cost of loss of scrutiny of the company in the public light?

The above concerns are the pinch(es) of salt that you must take with this euphoria of SPACs we are currently going through, the question boiling down to, whether SPACs are blank checks or blind faith!?