Categories

A needle prick and a drop of blood, what can they tell really?

Once upon a time, a silicon valley darling claimed a drop of blood, a magic box and a revelio charm could unravel a wide variety of diseases (Potter heads, get it?). The founder of Theranos liked to call her blood testing system the iPod of healthcare. But unlike iPod, an entire industry was hoodwinked into believing a false tale, before the startup failed atrociously. The fall from the pedestal was also financially steep for Elizabeth Holmes, who’s net worth was estimated to be $4.5B in 2014 and zero by 2016. Pensive investors got more reluctant to hedge their bets and the industry of blood diagnostics, especially point of care testing (PoC) was set behind by decades. (For a riveting in-depth critique of Theranos, I would recommend checking out Bad blood by John Carreyrou.)

“ Point of care testing refers to rapid, reliable diagnostic tests performed outside labs

While point of care testing took a beating, within the world of medicine, clinical lab tests (here we define it as, tests conducted on patient biological samples within a lab setting) play a critical role in diagnosis. Infact, 70% of medical decisions depend on laboratory test results!

Blood, saliva and samples of ‘stuff’ that shall not be named open up an entire world of Narnia. Much like Narnia, there are doors, lamp posts, fantastical creatures and witches.

In case of a blood test, a door represents analyzers (various instruments, chemicals, reagents etc.) that are used to peek into the microscopic world. Then there are lamp posts, basic tests that indicate your general health and the potential direction its heading. For example, the late night Ben & Jerry’s for the past month has led to spiking of sugar level. It’s time to stop adding Ben & Jerry’s to your grocery list. Speaking of fantastical creatures, there is now increasing evidence that your blood sample is teeming with very much alive microorganisms, which can again tell a lot about your overall health. Unfortunately there are witches too – cells gone rogue, infected or simply tired. A tangible evidence of a certain disease state, using which and many other parameters your clinicians put together a treatment plan. Voila! That’s how clinical lab tests are at the front and center of one’s medical diagnosis.

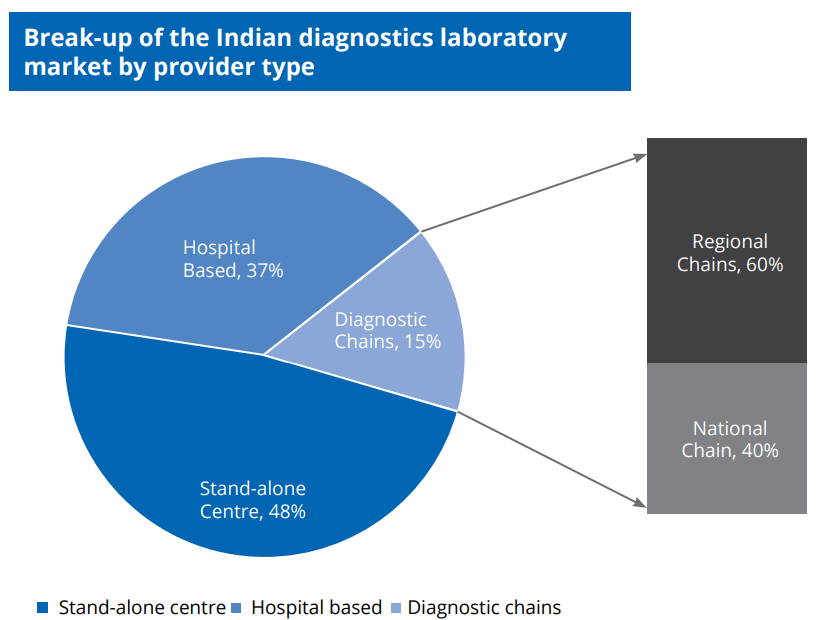

Now that we know the lay of the land, let’s take a hard look at the clinical lab diagnostics industry. Clinical diagnostics is expected to rake in >$300B globally by 2028, an incredulous ~60% growth compared to 2021. Indian clinical labs represented 3% of the market, i.e. $6B out of the global total of $193B in 2021. Out of ~100,000 labs in the country, only 1% of them have NABL accreditation.

Overall this highly fragmented (45% are standalone centers), mostly unregulated market is driven by high volume, low cost tests. Typically these tests account for a low 12-15% of total cost of hospitalization in both urban and rural hospitals. The gross margins are starkly different – for unorganized (standalone & hospital based) it can be anywhere between 30-45%, while for organized diagnostic chains, 40-60% is achievable owing to economies of scale.

During the pandemic, if there was ever an industry that took center stage along with pharmaceuticals (mostly for good reason), it has to be this! Analysts even claim that COVID testing brought in $30B for clinical labs worldwide, with the Indian clinical diagnostic sector seeing more than 20% growth in topline (FY22). New pandemics are only imminent, combined with a growing population, increasing life expectancy, higher incidence of chronic diseases and the beginnings of the wellness testing wave, means that clinical labs are seeing some serious tailwinds tugging them forward.

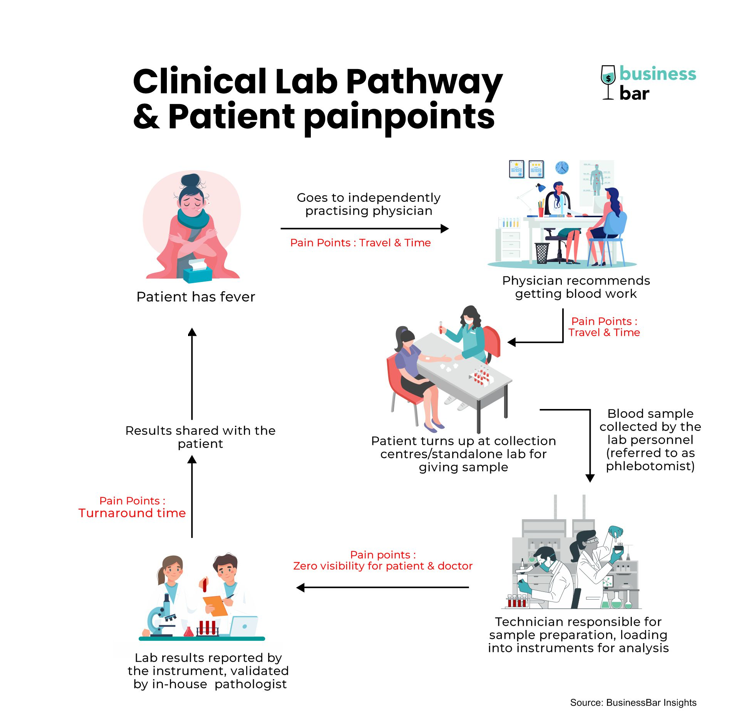

The billion dollar question then is, are the labs up for the challenge? More specifically, are the Indian pathology labs ready to cater to evolving needs of the great billion? Let’s look at a typical patient experience at a lab operating in a Tier 1 city, which does not heavily invest in digitisation.

Familiarity often has an interesting way of obscuring broken pathways. In the scheme of everyday things, where we as consumers expect the best experience, clinical diagnostics today falls short. It has no/abysmally low levels of end to end digitization. From the outside world, it does not seem comparable to a consumer experience of a Zomato order, a Flipkart purchase or an UPI transaction. Perhaps we are missing something!

For a country that has leapfrogged in various sectors, is it really possible that the fate of the clinical laboratory is doom and gloom? Maybe there are certain upstarts that are altering the patient journey in a way that can fill us with hope.

(Hopefully Lao Tzu doesn’t mind me reinterpreting his famous quote)

Patient – Doctor Interaction: Is it possible to get a physician’s opinion without traveling to their clinic?

Absolutely! A fully digital consultation is very much a reality today. For urban India, startups like Practo, Lybrate, Docsapp made digital doors to doctors possible. So much so that a pre-pandemic report claims that telemedicine in India has the potential to reduce in-person outpatient consultation by half by 2025. Could this be a reality we wake up to in 3 years of time? Sounds highly optimistic!

As of today, two things are clear:

A. There is a digital front door access to clinicians in urban India

B. It is unlikely that this door will shut down forever or that brick and mortar clinics will wither away either

Patient – Lab Journey: Does this digital door extend into clinical laboratories ?

Most of the tele consult startups recognize that consultation does not happen in isolation in the real world. They have fervently incorporated e-pharmacy, laboratory diagnostics, nursing, physiotherapy services etc. into their business models. Each one of them frantically trying to find revenue streams that supplement their business.

Zeroing in on laboratory diagnostics, after a virtual consult can the lab tests be done remotely? Short answer, no. Long answer, certain elements of the process are becoming more accessible.

For instance, basic tests can be done via a PoC device. The quintessential example being that of a glucometer, used to measure blood glucose level or rapid pregnancy tests. More recently – remember, yours truly the COVID test kit? PoC devices are evolving constantly and there are several new trendy kids on the block including the likes of Ultrahuman glucose patch. Yet, the most critical shortcoming is that despite much R&D underway, the self-test menu offered by these devices aren’t broad and complex enough to meet every patients’ needs. (For the tech nerds, check out the fantastic TechCrunch review as Ultrahuman Cyborg)

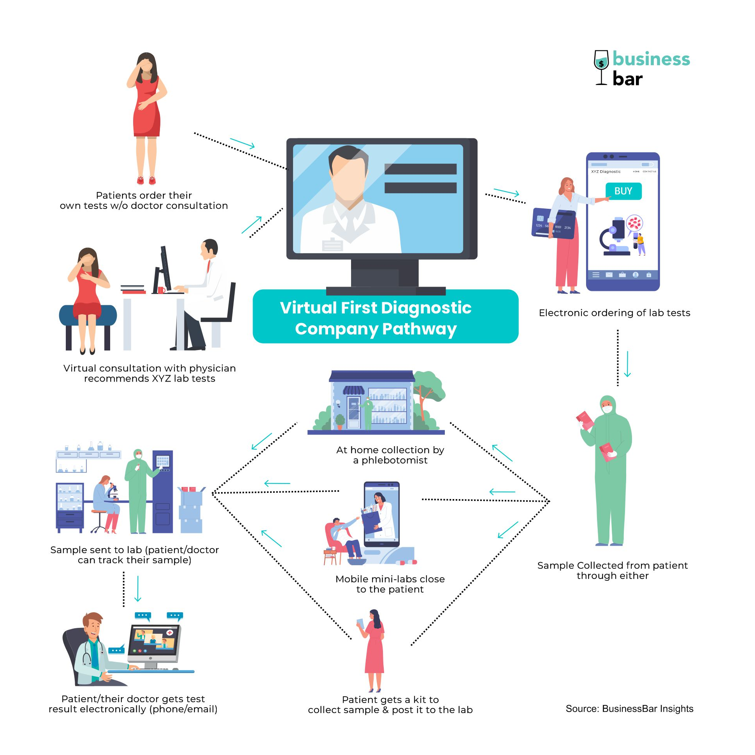

Diagnostic startups are therefore stepping up their game to increase accessibility of the digital door into more complex tests. Today we shall look into one of them – those that operate on the motto of, if you can’t come to the lab, either the lab technician or the lab come to you, aka virtual first diagnostic company.

For a virtual first diagnostic company to be truly customer centric, it has to be able to optimize three levers – acquiring customers, sample collection, sample analysis and reporting. Don’t let the trifecta fool you into thinking that it’s a simple feat – there’s way more than what meets the eye.

Acquiring customers: The demand comes from consumers & doctors who are looking for either wellness or sickness tests. Healthians, for example, relies primarily on health proactive consumers from 250+ cities in India to go online and book their lab tests, a direct-to-consumer model. On the other hand, Orange health depends on clinicians as primary clients, who book lab tests for their patients and can track results on the app. Their thesis being that since 90% of tests in India tend to be sickness tests prescribed by doctors, doctors ought to be an integral part of the distribution channel. (Yuvraj Singh has invested in Healthians – check out our article on celebrity investors here).

Sample collection: Going back to our earlier example, Healthians has a fleet of 2500+ phlebotomists who come to your doorstep to collect your sample for free. Recently, they have also begun to experiment with mobile mini-labs under the banner name of “Health on wheels” in the Delhi NCR & Mumbai region.

For this vertical of the business, our hypothesis is that unit economics is the biggest barrier. The price differential of lab tests offered by virtual first diagnostics companies tend to be at least 30% lower to their traditional competitors. For example, a lipid test that might typically cost INR 600-800 at diagnostic centers is offered at ~INR 200 by virtual first diagnostic companies.

While this helps in customer acquisition, the low value of tests cannot offset a much higher cost of collection compared to a Zomato drop off. Ultimately, leading to laser thin margins for this vertical of the business. It’s therefore likely that virtual lab service providers operate mobile phlebotomy/at home collection at a loss to upsell and/or acquire new customers. Scale is the only plausible way out of the thin margin quagmire. However, we now know that it’s easier said than done. Don’t even get us started on the undersupply of phlebotomists (0.0078 per 1000 people) and the necessity to transfer samples in a safe manner to testing labs.

Sample analysis & reporting: Sample analysis & reporting is one of the ultimate determinants of success in this industry. Inaccurate test results and late turnaround times (TAT) dry up digital customer queues faster than the Thar desert in summer.

Once the sample is collected, it is crucial to either have a close proximity network of lab/partners and logistics to mitigate sample degradation. Once the sample reaches the lab, it is prepared and loaded into the instrument by a lab tech – analyzed by the instrument – results are validated by the pathologist and reported electronically back to the customer.

The composition of the lab network as Marrissa explains in this fantastic piece on Diagnostics as a service is perhaps the biggest clinical risk! And with good reason.

To acquire or to build; that is the question.

For virtual first diagnostic companies to reduce their real estate overheads, it makes the most sense to either: Partner with an existing lab/s as their lead generation entity or rent out the space of an existing loss making lab/s and take over the business as their own. The latter means more control, but that comes with the need to expand on the core competencies of the company.

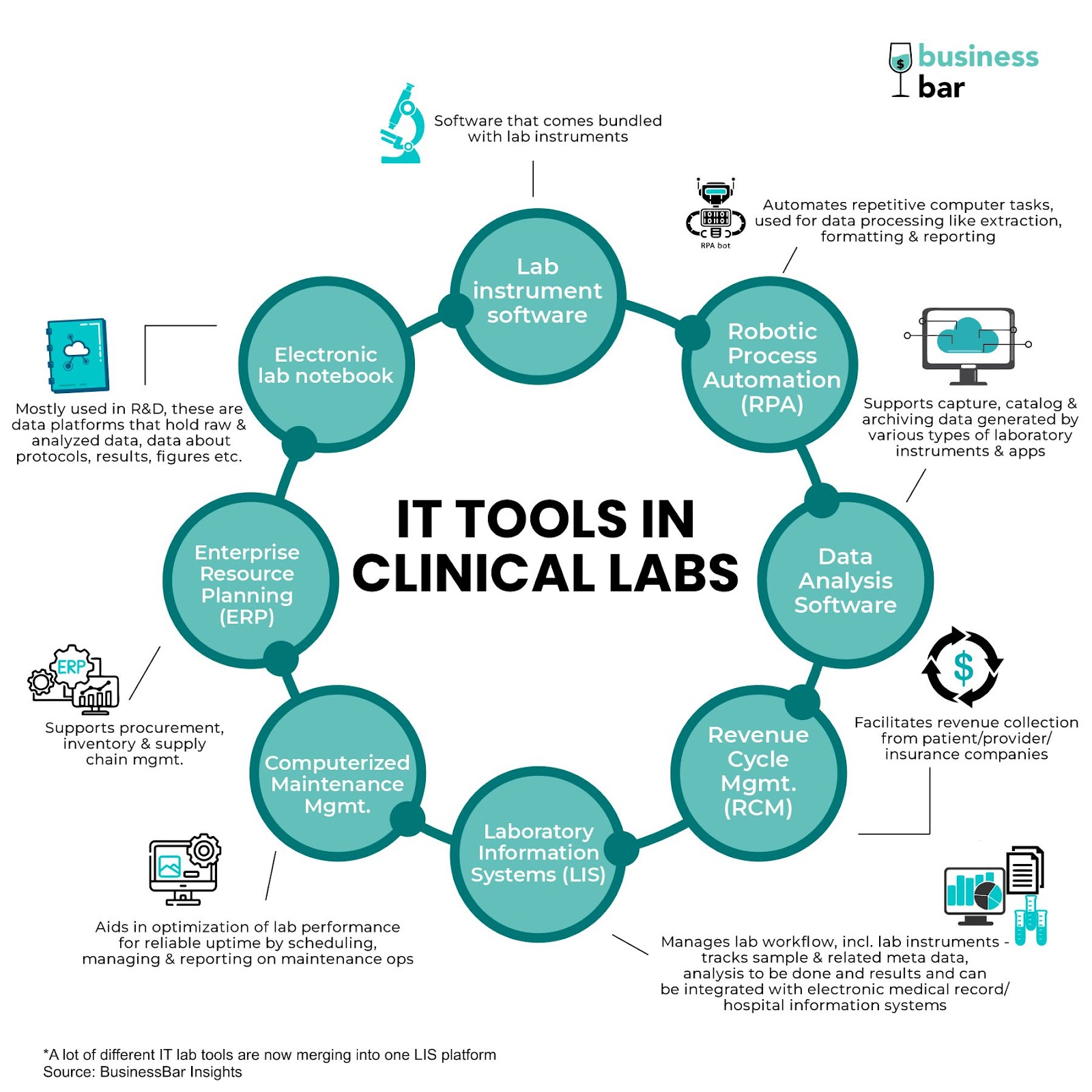

What does it take for a lab to churn out quality accurate results with short turnaround times? Well trained staff, standardized protocols, reliable instruments for sample analysis and a high degree of automation of clinical and non-clinical tasks.

The good news is that – a conversation with a lab owner on “How to run clinical labs 101” might as well open up an entire playbook. You will notice however that the critical IT tech chapter tends to have more than a few missing pages. A virtual first diagnostic company cannot afford to keep repeating the same manual clinical and non-clinical tasks, as that of a traditional lab.

Startups like Healthians & Orange health are more than eager to showcase the implications of deeper tech integration. If you have got it, you flaunt it! Healthians recently activated live tracking and Orange health promises 6 hrs. of TAT for blood samples and 9 hrs. for COVID.

Although the name of the game being volume holds true for a traditional diagnostic chain, it is even more so for a tech enabled one. Tech can enable transparency & efficiency, subsequently translating into short TAT, customer love which equals more customers and therefore, bigger topline.

Behind the scenes, the cost of the business can scale down disproportionately quickly with these volumes. Different IT tools used within a lab, can effectively bring down 85% of cost attributed with running the real-estate part of the business (rent/lease of lab space & instrument, manpower, reagents and other overheads) by efficiency gains and the remaining, via digital marketing/sales tools that have opened up opportunities for optimizing cost of customer acquisition (CAC). Whether these tech enabled virtual first labs can attain positive EBITDA margins remains to be seen.

Let’s run some numbers shall we? There are 1.4 billion people in India. Approximately 90 million live in the major metropolis, which is the playground for these new age virtual diagnostic companies. In totality, the two big competitors, Orange health and Healthians have served ~4M people over the years. Add in another million for other local virtual first startups, that still translates to mean 5% of people living in the urban metropolis have availed their service. 0.4% of the total Indian population, to be exact.

What does this tell us?

Are there digital doors into the clinical lab sector? Yes there are.

Do they have more digitized laboratory back offices? You bet!

Are they truly digital when consumer facing? For most part, but they do also operate through aggressive telemarketing.

Have they penetrated the larger Indian healthcare ecosystem? Not yet and not even close.

The way we see it, virtual first diagnostic startups are yet in their early phase of tackling the needs of this massive population. What they are doing however is beginning to democratize access to these tests, an equalizer of sorts.

The best part? They are slowly morphing and building up the modern consumer journey of a 21st century India within the clinical diagnostics industry.