Categories

It’s 2019, and the high-end shopping streets of Paris are bustling with tourists trotting in their Jimmy Choo heels, wearing their Louis Vuitton outfits, and sporting their Gucci Bags and Rolex watches. All while their assistants follow them – struggling to carry their innumerable shopping bags to their newly bought Lamborghini. Everything about them speaks of glamour, glitter, and well – money!

Mainstream media often presents this romanticized larger-than-life picture of fashion, luxury and shopping. Movies and shows like Pretty Woman, Sex and The City, and the more recent Emily in Paris, come to mind. Time and again, these brands have also found their mentions in several Bollywood and Punjabi songs. And while we accept that these are often exaggerated representations of reality, there must be a reason why they seem to work their magic in the viewers’ minds.

You see, these multimedia representations sell rose-tinted dreams to the audience. Products and experiences that are only accessible to the uppermost rung of society automatically become conventionally desirable.

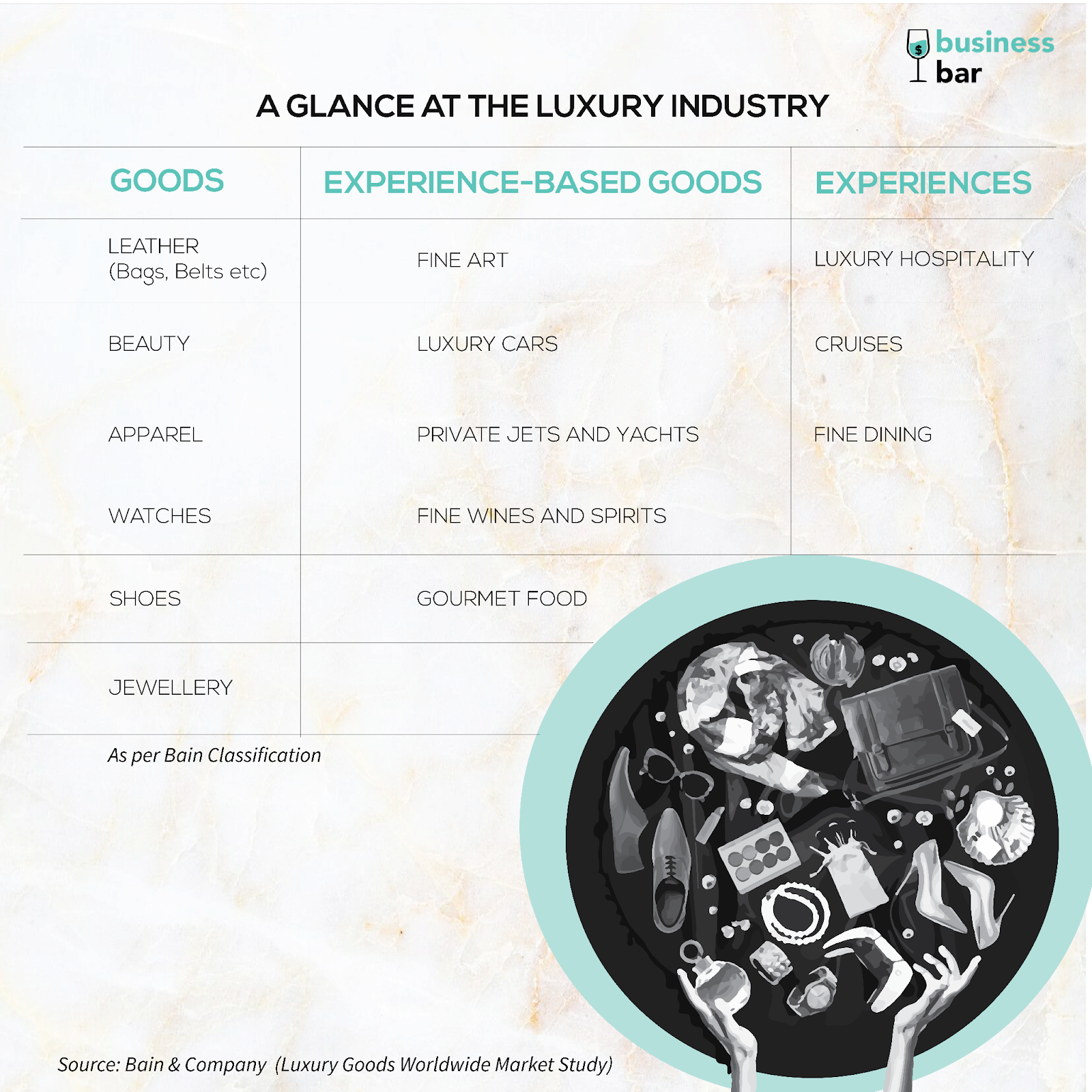

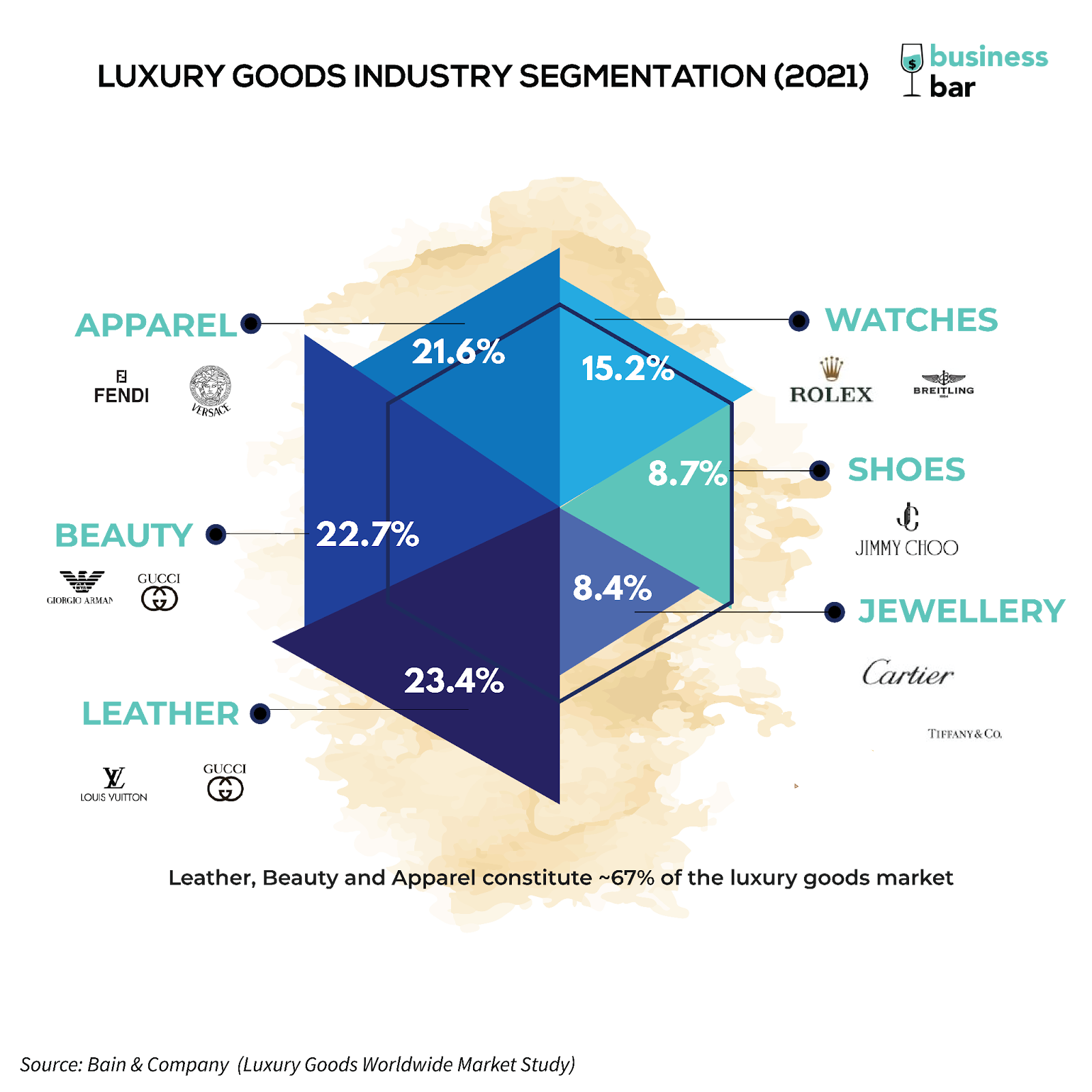

All these luxury fashion, cosmetics, fragrances, watches, jewelry, luggage and handbags together comprise the luxury goods industry. As one might expect, the industry has predominantly been dependent on the extent of travel, tourism and sales from the fancy brick-and-mortar showrooms. So it is no surprise that the industry plummeted when COVID-19 hit.

Who would care about luxury goods and experiences when humanity is going through a pandemic, right?

Well, how then, in the midst of all this, did Bernard Arnault, the chairman and CEO of LVMH (Louis Vuitton Moët Hennessy), manage to become the wealthiest person on the planet, briefly in 2020 and then again in 2021? As of writing this article, he maintains his position as the 2nd richest person globally with a net worth of USD 194.6 Bn (sandwiched between Elon Musk and Jeff Bezos, by the way! ).

Clearly, there’s more to the story.

In recent years, the luxury goods industry has undergone some fundamental changes – everywhere from the evolving customer behaviour to emerging geographies to the luxury brands’ slow yet much-needed acceptance of digitalisation. The pandemic only accelerated these changes.

Let’s look at how the industry has fared through COVID-19 and discuss some emerging trends that will shape the industry in the upcoming years.

The luxury goods industry lies at the core of the overall luxury industry, which includes goods, experiences, and experience-based goods.

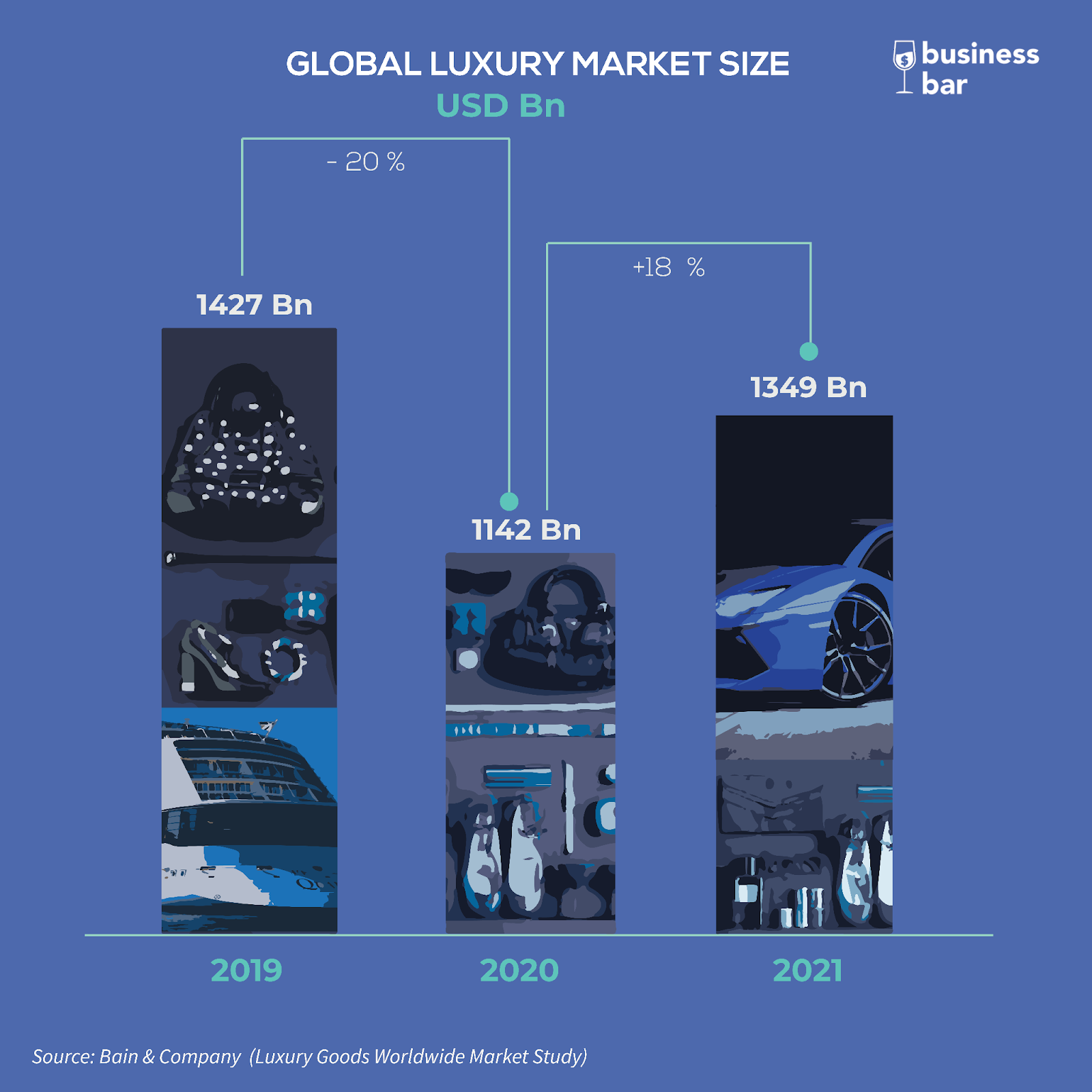

In 2019, the overall luxury market was sized at a whopping USD 1.44 Tn (greater than the GDP of Australia), and growing at a steady ~8% CAGR from 2010-19. With the onset of the pandemic, the industry dropped down ~22% from the 2019 levels, with some segments showing a steeper drop than others. While the luxury goods segment and experience-based goods segments declined by ~21% and ~10%, respectively, the luxury experiences segment was disproportionately impacted (~56% decline) given its reliance on travel.

The recovery through 2021 hasn’t been uniform across the segments either. In 2021, the luxury goods and experience-based goods bounced back to their pre-pandemic levels, but the luxury experiences still remained far below 2019, and understandably so. Several studies have indicated that the consumer appetite for travel is at an all-time high. Hence, it wouldn’t be unreasonable to expect an accelerated recovery of luxury experiences once the travel restrictions are relaxed.

The industry’s prompt rebound comes as a surprise to many. One should note that the recovery was offset due to an entirely new set of emerging consumer trends, quite different from the ones that the luxury industry had grown traditionally accustomed to.

The luxury goods industry finds its roots back in the 1800s when the first luxury fashion houses Hermès (1837) and Louis Vuitton (1854) were established. Over the 19th and 20th centuries, many other luxury conglomerate groups like Prada, Richemont, Kerling etc., have mushroomed.

The industry has been inherently dynamic with frequent mergers & acquisitions.

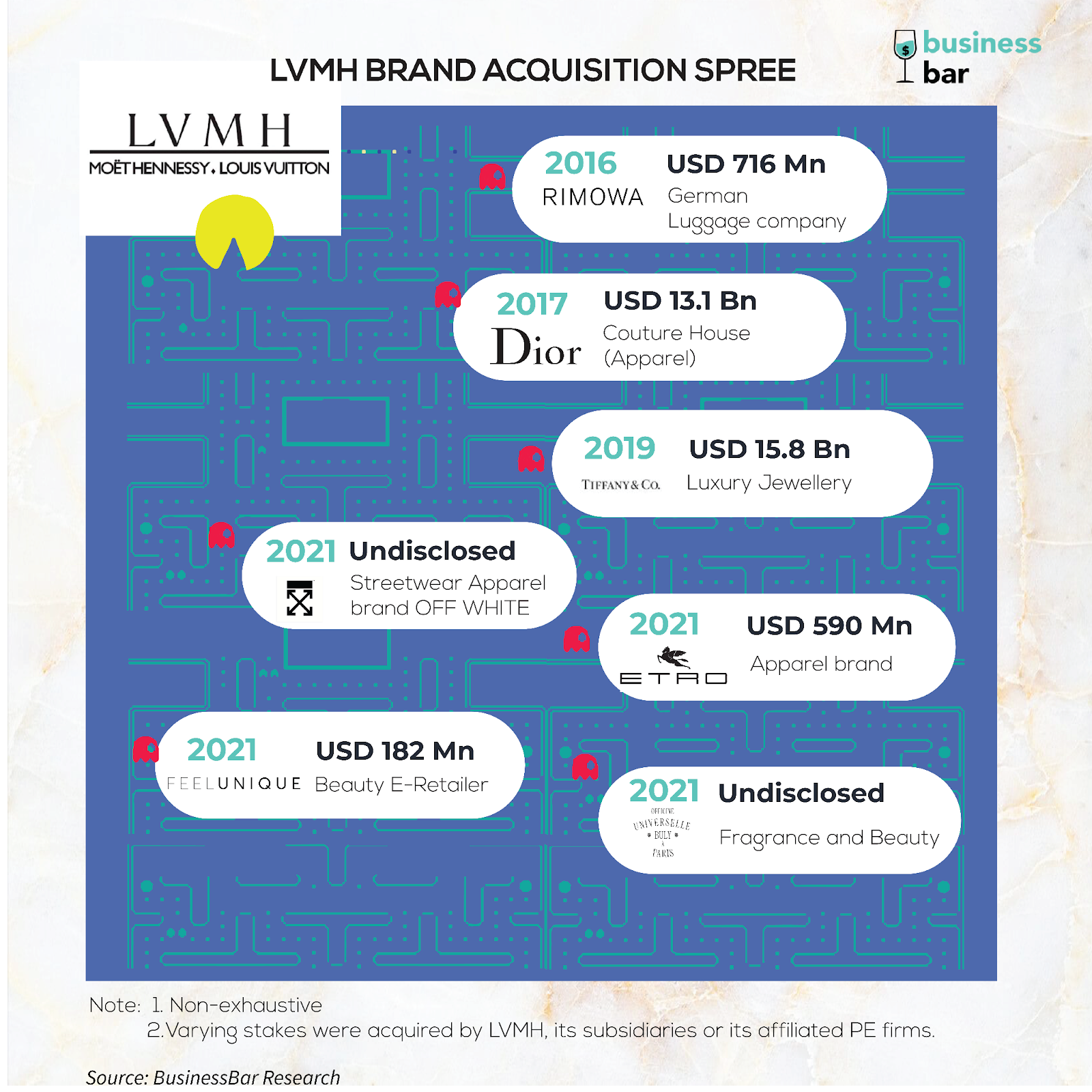

Let’s take Louis Vuitton’s parent company LVMH for instance. At present, LVMH owns over 75 luxury brands across all segments of the luxury industry – ranging from apparel, beauty, jewellery to fine wines & spirits and even luxury hotels. The group reported a record USD 71.5 Bn revenue in 2021, and its market cap stands at USD 393 Bn as of writing this article. This makes it the most prominent luxury conglomerate in the world and the largest company in Europe.

Over the last decade, the group has been on a spree of acquisitions across all luxury goods categories.

And if all that was not enough, in 2019, LVMH also collaborated with the famed pop star Rihanna to launch a full-fledged fashion line called Fenty. The joint venture where Rihanna owns a 49.99% stake (LVMH owns the remaining 50.01%) made her the first woman of colour to lead an LVMH label. One might argue that it also catapulted her to the status of a billionaire. (Fenty was eventually put on hold in February 2021)

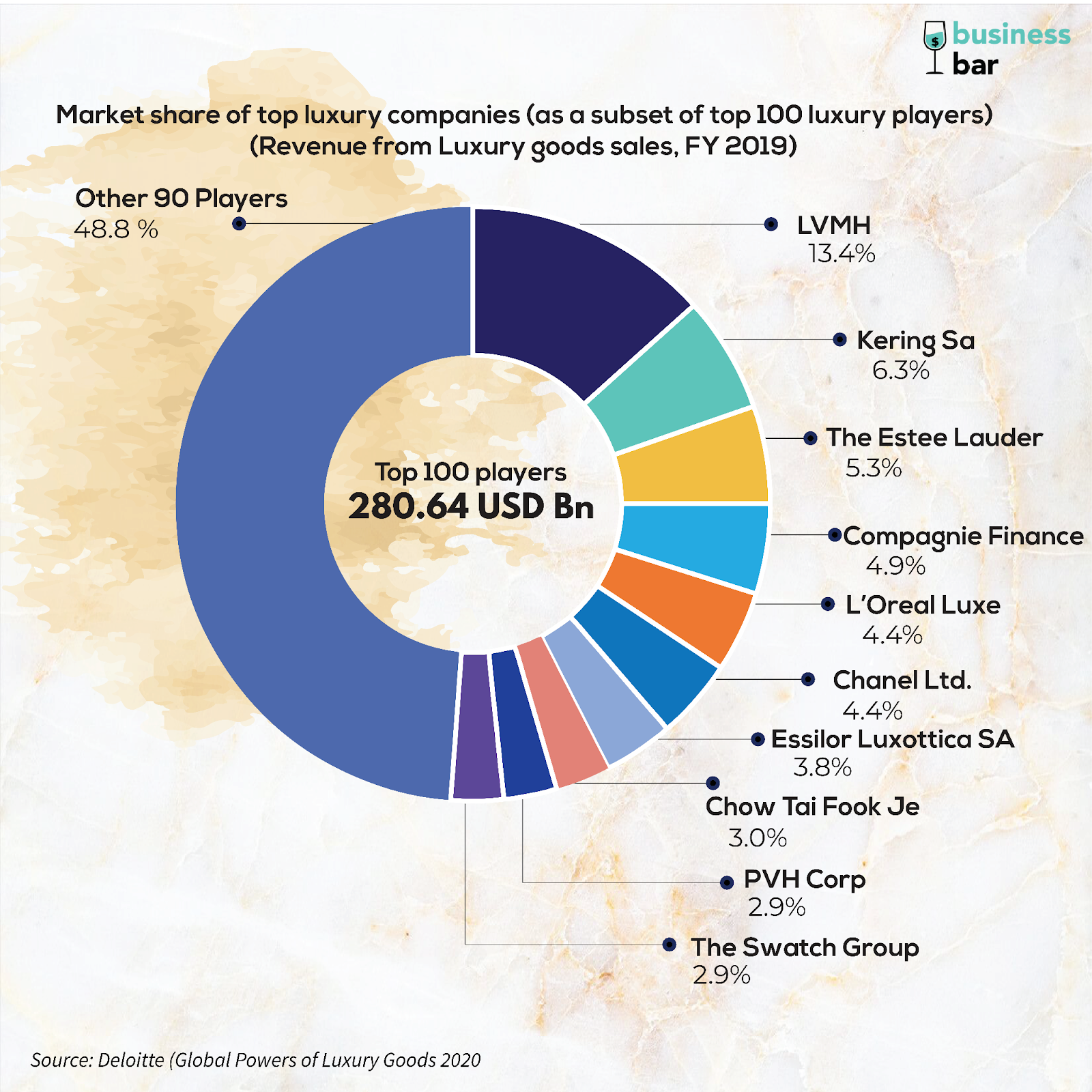

Such frequent mergers and acquisitions have been happening across the industry, causing it to consolidate. In FY19, within the top 100 players, the top 10 accounted for 51.2% of the total sales and 71.7% of the total profits.

Now that we have all our basics covered, let’s dive straight into the trends that are reforming the luxury goods industry as we speak.

China is a country that finds its mentions everywhere – and the luxury industry is no exception. China’s economic growth over the past two decades has been nothing short of a spectacle. The Chinese economy is the second-largest globally, recording a massive GDP of USD 18 trillion in 2021.

And this growth is clearly reflected in the consumption patterns of its citizens. The average annual income tripled from 2010 to 2020. Estimates show that the number of households in the upper-middle-class income is projected to grow by 68% from 2020 to 2030.

All this means that Chinese people have more to spend, and spend they will! By 2019, Chinese customers accounted for almost a third of the global luxury goods market. Much of this spending was contributed by shopping sprees of Chinese tourists travelling abroad.

Statistics show that as many as 169.2 Mn Chinese people travelled abroad in 2019. And so understandably, while Chinese customers spent more on luxury goods than consumers of any other nationality, the spending within China (geographically) only accounted for ~10% of the market.

But this was soon to change! As lockdown was imposed and travel banned – more and more people turned to domestic spending. As a result, the share of luxury goods spending in China almost doubled to ~21% in 2021. And China is leaving no stones unturned to make this shift a permanent one.

As a part of its ‘dual circulation strategy’, China is aiming to boost the economy with higher domestic consumption. Duty-free shopping is a crucial chess piece to make that happen. Plans are in place to develop duty-free shopping complexes in 5 prominent cities (Beijing, Shanghai, Guangzhou, Tianjin and Chongqing) to attract investments by international brands. Meanwhile, the Chinese province of Hainan is already on track to be the shoppers’ mecca, given its duty-free provisions.

If China is able to keep up this momentum of Chinese people spending locally, it is likely on course to become the largest luxury goods market in the world by 2025.

As you might have guessed already, it wasn’t only the Chinese that turned local; consumers worldwide also turned to shop domestically. And that is how luxury went local!

A brick-and-mortar store allows the luxury brands to shower the customers with gestures of grandeur, reinforcing their messaging of exclusivity through every single inch of the store. From the choice of wine served to the way a staff member speaks – everything is designed to deliver the epitome of customer service. This customer experience simply cannot be replicated through e-commerce deliveries. And so, for the longest time, the luxury brands have been reluctant to go online.

While the brands had adopted digital marketing to some extent by 2019, they majorly relied on physical sales through mono-brand stores or third-party multi-brand stores. However, 2020 presented an unparalleled dilemma – to adapt or to concede.

The pandemic paved the way for the emergence of a host of luxury e-commerce platforms. Not only have the brands promoted sales through their mono-brand/ multi-brand websites, pureplay multi-brand e-tailers and marketplaces have also been established. Marketplaces like Farfetch and Net-a-Porter (Richmont owned Yoox Net-a-Porter Group) dominate Western markets. Meanwhile, Alibaba’s Tmall Luxury Pavilion has emerged as a leading marketplace in China. Resale platforms like Vestiaire Collective have also gained significant traction of late.

The share of online purchases in the luxury goods market has gone up from 12% in 2019 to 22% in 2021. More than 90% of the customers now experience some digital touchpoint before making their purchase. Even though they might buy the product in person, their choices are highly influenced by digital discovery.

In an attempt to maintain the levels of customer delight, luxury brands have adopted several measures. Some of these include digital showroom tours, private online consultations, exclusive products live-streaming with influencers and brand ambassadors, curated complimentary gifts etc. The largely positive response is a strong indicator that the online channel is all set to grow and account for ~30% of all luxury goods sales by 2025.

These digital offerings have also unlocked an untapped market for luxury brands – the younger generations of shoppers.

It wouldn’t be exaggerating to say that today’s youth are under immense social pressure. Influence or influenced? Fit in or stand out? – these are the questions they’re asking themselves.

At the same time, they’re often looking for something they resonate with, something that sets them apart – and they’re willing to pay for it.

In 2019 the Gen-Z represented a modest 8% of the luxury goods purchases. However, they’ve quickly grown to represent 17% of the market in 2021 and are expected to account for ~40% of the sales by 2035. This expedited growth is contributed partly by the rising income levels and the increased accessibility of luxury brands online. As soon as 2025, the millennials and Gen-Z are together projected to comprise almost 70% of the market.

These younger cohorts of shoppers come with a unique set of behaviours. Their purchase decisions are influenced by their favourite celebrities and influencers. Unlike the older generations, they are more likely to consider the resale value of these luxury products. They have high adoption of social media and digital innovations. The intersection of unique styles and products, with incredible stories, takes precedence over brand heritage and history.

Luxury brands have taken notice.

Brands are increasingly collaborating with popular youth icons in innovative ways. For instance, Saint Laurent, a french fashion luxury house, collaborated with Travis Scott, the famous American rapper and singer, to release limited-edition music. The physical copies of the music tracks were designed by the creative directors at the fashion house. Brands are also going beyond just mainstream celebrities and collaborating with young leaders from diverse backgrounds to send out a message of inclusivity and establish a connect with the younger audience. The industry is slowly shifting from exclusivity towards uniqueness.

Luxury products are just one form of self-expression for today’s youth. They want to consume products that resonate with their values and promote the environment and social responsibility.

In the past, the luxury goods industry has been notoriously known for its unsustainable and environmentally polluting practices.

The media has highlighted instances of large scale burning of unsold inventory by luxury brands to maintain their perception of exclusivity. In 2018, Burberry, a British luxury fashion house, was catapulted to fame and not for the right reasons. It was revealed that the brand burned USD 38 Mn worth of products using specialist incinerators in 2018. And over the years, multiple luxury brands have been accused of endorsing this practice. In 2019, as the world’s luxury capital, France became the first country to ban the burning of unsold luxury goods to solve for the sweeping environmental impact.

Over the recent years, an increasing number of luxury brands have also started to incorporate sustainability into their philosophy. There has been an industry-wide focus on concepts like ethical fashion (production methods and working conditions), circular fashion (recycling, upcycling, and thrifting), slow fashion (sharing, renting), and conscious fashion (eco-friendly and green fashion).

Luxury brands are investing in innovation to develop sustainable materials to replace leather and fur. For instance, in 2018, Stella McCartney launched a series of cruelty-free vegan ‘Flabella bags’ made from lab-grown Mylo mushroom leather. Similarly, Chanel has invested in Evolved by Nature, a US-based biotech startup, to develop silk sustainably.

We all know that the focus on sustainability is here to stay. There’s a long way to go, and it is hopeful to see the mainstream luxury brands contributing their bit towards the journey.

We have seen that the luxury industry has been quite conservative in more ways than one. However, it is definitely not late for the Web 3.0 revolution.

Brands like Louis Vuitton, Gucci, Balenciaga and Burberry have already launched NFTs of their products and established their presence in the metaverse. Not only does this provide for a tool to verify authenticity and ownership – but it also presents an exciting opportunity for luxury brands.

With the gaming industry at an all-time high, these high-profile brands are leveraging NFTs to create digital skins for avatars in video games. The amalgamation of luxury and gaming is so powerful that in 2021, the digital version of a Gucci bag was sold at a higher price than the actual bag. It also presents an avenue for the brands to aggressively target the Gen Z consumers.

In reality, the impact of fashion gaming goes well beyond revenue creation. Gaming provides an innovative solution to the luxury industry’s sustainability problem. By launching virtual-first products, the brands can evaluate customer interest and gather feedback – all before they manufacture the physical product. Through this improved mechanism of demand estimation, brands will be able to manufacture physical products that they already know will be successful – thus solving the problem of the unsold inventory (and its aftermath burning).

Clearly, Web 3.0 is already opening doors for the luxury industry that would have been beyond imagination just a few years ago. And this is only the beginning. The world is swiftly moving to the Decentraland and judging by the current scenario, the future of luxury looks extremely promising.

Notice how the broad underlying themes of localization, digitalization, shift towards younger customers, emphasis on sustainability and adoption of Web 3.0 repeatedly tie back to each other. And the intersection of these trends is giving a whole new meaning to luxury. It wasn’t very long ago when the luxury industry was known to be conservative and traditional in its mannerisms. Today it is quickly becoming a front runner in innovation and agility. It has conformed and adapted to the changing world and the evolving consumer demands – all while carving out a sweet spot for itself. And as long as humans continue to crave indulgence and feed off materialism, it is safe to say that the luxury industry will continue to strive and thrive!

Co-written with Rutvi Narang